ETFs focusing on energy, oil services, and cannabis were top performers in October.

Top Performing ETFs for October 2022

Excludes ETFs leveraged or less than $500 million in assets

* VanEck Oil Services ETF, OIH +41.4%

* Energy Select Sector SPDR, XLE +25.0%

* Fidelity MSCI Energy Index ETF, FENY +24.3%

* Invesco S&P 500 Equal Weight Energy ETF, RYE +24.2%

* AdvisorShares Pure US Cannabis ETF, MSOS +24.1%

Stocks contributing to the performance of the above ETFs likely include ChampionX (CHX), Chevron (CVX), ConocoPhillips (COP), EOG Resources (EOG), Exxon Mobil (XOM), Green Thumb Inds (GTBIF), Halliburton (HAL), Helmerich & Payne (HP), Marathon Petroleum (MPC), Patterson-UTI Energy (PTEN), Phillips 66 (PSX), Schlumberger (SLB), Trulieve Cannabis (TCNNF), and Valero Energy (VLO).

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks came under pressure last week after Fed Chair Powell dispelled any notion of slowing the pace of interest rate increases. Employment indicators continued to portray resilience. Investors will focus on the outcome of the midterm elections and October consumer price index data this week.

The Federal Reserve raised the benchmark federal funds rate by 0.75% last week to the 3.75–4.00% range. Chairman Powell said that the Fed’s inflation fight is far from over and that it is “premature” to discuss pausing interest rate increases.

Powell also said the economic data since the September 20-21 Fed meeting suggest that the “ultimate level of interest rates will be higher than previously expected.”

The economic data that came out last week did little to alter the above expectations. The job market continued to be resilient and overshadowed any weakness in manufacturing.

The Labor Department reported the economy added 261,000 jobs in October, topping economists’ forecast of 205,000. Average hourly wages increased by 0.4%, exceeding economists’ 0.3% estimate. The unemployment rate rose to 3.7% in October from 3.5% in September.

The Bureau of Labor Statistics reported that job vacancies increased by 500,000 from August to 10.72 million in September.

In other economic data, the Institute of Supply Management’s manufacturing index fell to 50.2 in October, its lowest level in nearly 30 months.

Stocks came under pressure as bond yields rose in response to Powell’s comments on the outlook for interest rates. The S&P 500 fell below its 50-day moving average.

For the week ending November 04, the S&P 500 (SPY) fell 3.3%. Three of the 11 sectors advanced.

Energy (XLE) gained the most, while communication services (XLC) lost the most.

Leading and lagging sectors for the week ending November 04, 2022.

The S&P 500’s top 10 winners included the following:

1. Health Care Sector

Abiomed (ABMD) +45% – The week’s top performer in the S&P 500.

Hologic (HOLX) +12%

2. Consumer Discretionary Sector

Wynn Resorts (WYNN) +21%

Las Vegas Sands (LVs) +8%

Aptiv PLC (APTV) +8%

3. Industrial Sector

Boeing (BA) +11%

Johnson Controls Intl (JCI) +9%

4. Materials Sector

Freeport-McMoRan (FCX) +9%

Air Products and Chemicals (APD) +9%

5. Information Technology Sector

Arista Networks (ANET) +8%

Top ETFs for the week

The following ETF themes worked well: China tech, China, natural gas, copper miners, and silver. The top ETFs for the week include:

KraneShares CSI China Internet ETF (KWEB) 19.6%

iShares MSCI China ETF (MCHI) 12.2%

United States Natural Gas Fund, LP (UNG) 11.4%

Global X Copper Miners ETF (COPX) 9.9%

iShares Silver Trust (SLV) 8.6%

Midterm Elections and CPI in Focus

* Investors are looking ahead to the November 8th midterm elections, with the control of Congress at stake. Pollsters expect the Republicans to take control of the House of Representatives from the Democrats. While the Senate race is tighter, it too may be tilted in favor of the Republicans. A Republican-controlled Congress can curtail President Biden’s ability to pass the Democratic Party’s legislation after the midterm elections.

* Investors will get an update on the inflation reading when the Labor Department reports the October Consumer Price Index (CPI) on Thursday. Economists surveyed by Dow Jones expect core inflation, excluding food and energy costs, to rise 0.5% in October, a tad below the 0.6% recorded in September. Economists expect core inflation to increase by 6.5% for the 12 months ending in October, compared to the 6.6% increase recorded in September.

* The calendar of Federal Reserve officials is busy this week, with several regional bank presidents scheduled to speak. Investors will look for insights into how federal reserve officials perceive recent economic data and if a change in the size of interest rate increases could be in the offing.

* The third quarter earnings season slows with nearly two dozen S&P 500 companies reporting. Activision Blizzard, Becton, Dickinson & Co., Constellation Energy, Disney, DuPont de Nemours, and Occidental Petroleum are among the S&P 500 companies reporting earnings.

* Media outlets have reported over the weekend that Chinese health officials will continue to adhere to the current “zero-COVID” policy. The rally in commodities, spurred by hopes of China loosening its “zero-COVID” policy last week, could reverse this week.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Fidelity funds focusing on natural resources including energy and agricultural commodities, defense & aerospace, and insurance were top performers in October.

Top Fidelity Funds for October 2022

Excludes closed Fidelity funds

* Fidelity Select Energy Portfolio, FSENX +24.7%

* Fidelity Natural Resources Fund, FNARX +23.3%

* Fidelity Select Defense and Aerospace Portfolio, FSDAX +17.3%

Stocks contributing to the performance of the above Fidelity funds likely include Archer-Daniels-Midland (ADM), Bunge Ltd. (BG), Exxon Mobil (XOM), Hess Corp. (HES), Lockheed Martin (LMT), MetLife (MET), Raytheon Technologies (RTX), Schlumberger (SLB), Toro Co. (TTC), and Travelers (TRV).

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks rallied sharply last week as bond yields fell. Data from the manufacturing and housing industries showed higher interest rates having the desired effect of slowing economic activity. The Fed meets to set interest rates. Market participants expect the Fed to raise interest rates by 0.75% and slow rate increases after December. The October jobs report comes out on Friday. The third quarter earnings reporting season continues.

Stocks rallied sharply for a second week in a row as the yield on the 10-year Treasury note fell 0.19% to end the week at 4.02%. Economic data suggested that higher interest rates implemented by the Federal Reserve are cooling economic growth as desired.

S&P Global’s flash reading of U.S. manufacturing showed business activity contracting in October. The Purchasing Managers’ Index fell to 49.9 in October, its first drop below 50 in 28 months.

Housing data showed the industry bearing the brunt of higher mortgage rates. The Commerce Department reported a 10.9% drop in new home sales in September from August. Home prices fell 1.63% in August, as measured by the S&P CoreLogic Case-Shiller 20-City Index.

Meanwhile, the core personal consumption expenditure (PCE) price index, the Federal Reserve’s preferred inflation measure, rose 0.5% in September, in line with consensus economists’ forecast. On a 12-month basis, the core PCE index rose 5.1%, a tad below economists’ 5.2% forecast.

Investors expected the Federal Reserve to raise interest rates by smaller increments after December on account of the above economic data.

In third-quarter earnings, mega-cap technology companies, except Apple, lagged analysts’ EPS forecasts. Energy and healthcare company profits exceeded analysts’ expectations.

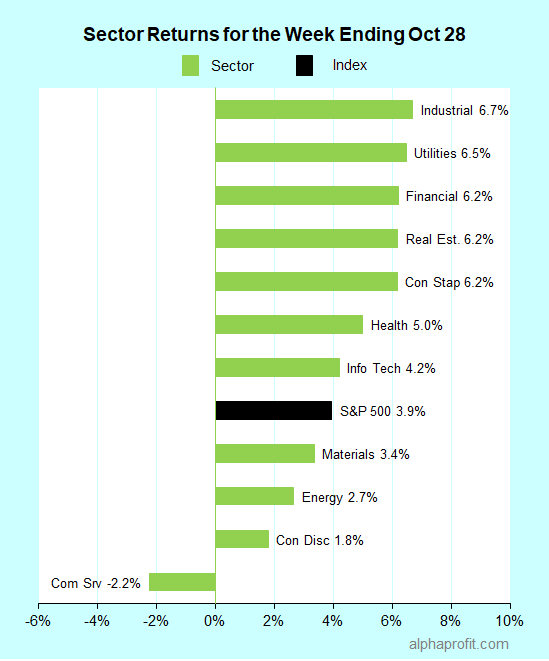

For the week ending October 28, the S&P 500 (SPY) rose 3.9%. Ten of the 11 sectors advanced.

Industrials (XLI) gained the most, while communication service (XLC) was the sole loser.

Leading and lagging sectors for the week ending October 28, 2022.

The S&P 500’s top 10 winners included the following:

1. Health Care Sector

Universal Health Services (UHS) +30% – The week’s top performer in the S&P 500.

DexCom (DXCM) +26%

Moderna (MRNA) +18%

Gilead Sciences (GILD) +17%

IQVIA Holdings (IQV) +17%

2. Information Technology Sector

Enphase Energy (ENPH) +21%

ServiceNow (NOW) +17%

3. Financial Sector

MSCI Inc. (MSCI) +18%

Raymond James Financial (RJF) +18%

Ameriprise Financial (AMP) +17%

Top ETFs for the week

The following ETF themes worked well: carbon credits, mortgage real estate, genomics & biotechnology, home construction, and smart grid infrastructure. The top ETFs for the week include:

KraneShares Global Carbon ETF (KRBN) 13.5%

iShares Mortgage Real Estate Capped ETF (REM) 11.2%

ARK Genomic Revolution ETF (ARKG) 9.8%

iShares U.S. Home Construction ETF (ITB) 8.9%

First Trust NASDAQ Clean Edge Smart Grid Infrastructure (GRID) 7.9%

The Fed Holds the Keys to Stocks Now

* The interest-rate policy-setting Federal Open Market Committee (FOMC) meets on Tuesday and Wednesday this week. Market participants expect the FOMC to raise the benchmark federal funds rate by another 0.75% at this meeting, taking it to the 3.75-4.00% range. The tone of the comments setting market expectations for the interest rate decision at the December meeting and beyond is likely to be more of a market mover.

* Investors will also get a pulse on the labor market when the Labor Department releases the October jobs report. Economists surveyed by Dow Jones expect the U.S. economy to have added 220,000 jobs in October, lower than the 263,000 jobs created in September. They see the unemployment rate nudging up to 3.6% in October from 3.5% in September. Investors will also watch the number of job openings with interest when the Bureau of Labor Statistics updates the data. The number of job openings contracted sharply to 10.05 million in September from 11.18 million in August.

* Another busy week of third-quarter earnings reports lies ahead. Eli Lilly, Pfizer, ConocoPhillips, Qualcomm, PayPal, Advanced Micro Devices, and Starbucks are among the S&P 500 member companies reporting earnings this week.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Better-than-expected earnings reports and hopes that the Federal Reserve could slow the pace of interest rate increases helped stocks overcome headwinds from surging bond yields and close last week with robust gains. Bond yields and mega-cap tech company earnings could determine if stock prices extend the rally to this week. An update to the Federal Reserve’s preferred inflation gauge is also due.

The S&P 500 managed to hold onto more than 2% gains made on Monday and Friday, finishing the week up 4.7%.

Bank of America reported stronger-than-expected third-quarter earnings, powering the advance on Monday. Hopes of the Federal Reserve slowing the pace of interest rate increases after November spurred the rally on Friday.

According to FactSet, 72% of the hundred S&P 500 companies reporting third-quarter earnings have exceeded analysts’ forecasts. Goldman Sachs, Netflix, and Schlumberger were among those that stood out.

Concerns about the Federal Reserve aggressively raising interest rates pushed the 10-year Treasury note yield to its highest level since 2008. The 10-year yield surged to 4.33% before pulling back to close the week at 4.21%.

The Treasury bond yield fell on Friday after the Wall Street Journal reported that some Fed officials would want to talk about slowing the pace of interest rate hikes after raising them by 0.75% at their November meeting.

Supporting this sentiment, San Francisco Fed President Daly said the Federal Reserve could begin to back off slightly from its aggressive pace of interest-rate hikes late this year.

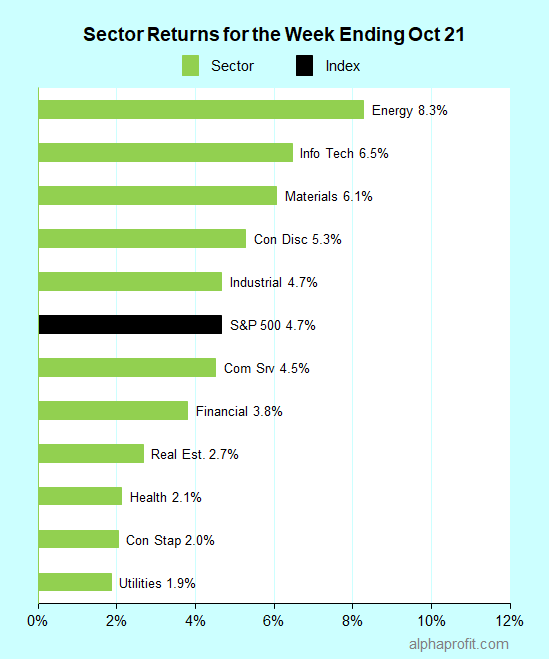

For the week ending October 21, the S&P 500 (SPY) rose 4.7%. All of the 11 sectors advanced.

Energy (XLE) gained the most, while utilities (XLU) gained the least.

Leading and lagging sectors for the week ending October 21, 2022.

The S&P 500’s top 10 winners included the following:

1. Communication Services Sector

Netflix (NFLX) +26% – The week’s top performer in the S&P 500.

2. Energy Sector

Schlumberger (SLB) +20%

Baker Hughes (BKR) +16%

Halliburton (HAL) +15%

3. Health Care Sector

Intuitive Surgical (ISRG) +19%

4. Information Technology Sector

Lam Research (LRCX) +17%

5. Industrial Sector

Lockheed Martin (LMT) +17%

6. Materials Sector

Freeport-McMoRan (FCX) +16%

7. Consumer Discretionary Sector

Carnival Corp. (CCL) +15%

Norwegian Cruise Line Holdings (NCLH) +15%

Top ETFs for the week

The following ETF themes worked well: oil services, Brazil, rare earth, metals, aerospace, defense, and Latin America. The top ETFs for the week include:

Will Bonds and Mega-cap Techs Help Sustain the Rally?

* The 10-year Treasury yield declined on Friday after gaining 0.30% from its October 14 close of 4.01%. This reversal has given hope that bond yields may have topped, albeit temporarily. A resumption of the increase in bond yields this week could derail the stock price rally that started last week.

* Earnings reports from the four biggest U.S. companies by market capitalization are due this week. Alphabet and Microsoft report on Tuesday, and Amazon and Apple report on Thursday. The four companies account for 20% of the S&P 500. The earnings reports should provide investors with information on how companies with dominant positions are coping against macroeconomic headwinds. They will provide investors with insight into the state of cloud computing, online advertising, consumer spending, and personal computing.

* Leading companies outside the technology sector that report this week include Boeing, McDonald’s, Caterpillar, Merck, and ExxonMobil.

* The September reading of the personal expenditures index is the eagerly awaited economic data for the week. Economists surveyed by Dow Jones expect the monthly rise in core inflation, which excludes food and energy prices, to moderate to 0.4% in September from 0.6% in August. They forecast core inflation to rise by a 5.2% annual rate during the 12 months that ended in September, up from 4.9% in August.

* The Bureau of Economic Analysis (BEA) releases its advance estimate for third-quarter U.S. GDP growth on Thursday. Economists surveyed by Dow Jones expect the U.S. economy to grow at an annualized rate of 2.4%, marking its first quarter of growth in 2022.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks gyrated wildly in the first week of the third-quarter earnings reporting season. The earnings reports failed to spur a sustained rally in stocks while inflation pressured them. The earnings reporting season picks up steam this week. The economic data calendar is light. Will earnings reports still be able to lift stocks, or will they steepen the slide?

Stocks swung between gains and losses as third-quarter earnings failed to lift stocks in the first week of the reporting season while inflation data pressured stocks.

Investors received updates on inflation in wholesale and consumer prices. The latter sparked an unexpectedly large rally in stocks.

The consumer price index, including food and energy costs, rose at an annual pace of 8.2% in September, compared to economists’ 8.1% forecast.

The core CPI, which excludes food and energy prices, rose 6.6% from a year ago. It topped economists’ 6.5% forecast by 0.1% too.

Stocks staged a remarkable turnaround after initially declining in response to the CPI data. On Thursday, the S&P 500 rose 194 points, or 5.6%, from its intraday low to its intraday high.

The surge, however, fizzled the following day after the University of Michigan’s consumer sentiment survey came out. The survey showed expectations for inflation over the next year rose to 5.1% from 4.7% in September due to higher gasoline prices.

Leading banks like JPMorgan Chase, Citigroup, and Wells Fargo joined Delta Air Lines, PepsiCo, and UnitedHealth to kick off the third-quarter earnings reporting season. The earnings reports failed to enthuse investors despite all six names topping analysts’ estimates.

FactSet data showed that 69% of the reporting S&P 500 members topped analysts’ third-quarter forecasts, trailing the 10-year average of 73%. The average earnings surprise was just 0.1%, compared to the 10-year average of 6.5%.

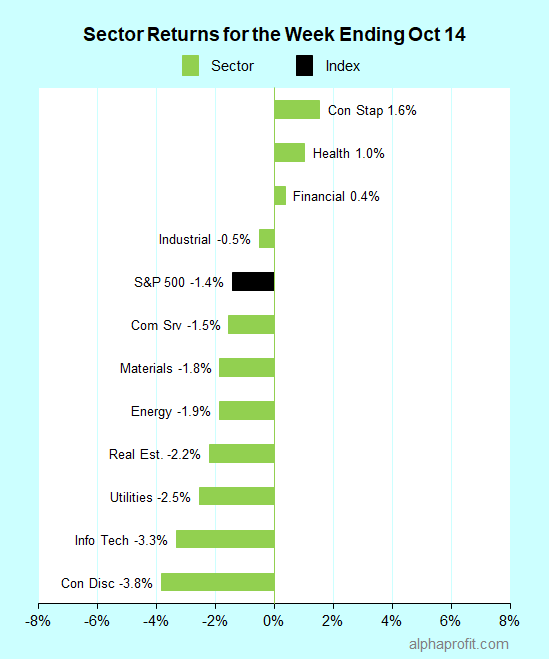

For the week ending October 14, the S&P 500 (SPY) fell 1.4%. Eight of the 11 sectors declined.

Consumer staples (XLP) gained the most, while consumer discretionary (XLY) lost the most.

Leading and lagging sectors for the week ending October 14, 2022.

The S&P 500’s top 10 winners included the following:

1. Health Care Sector

Moderna (MRNA) +12% – The week’s top performer in the S&P 500.

Amgen (AMGN) +10%

Viatris (VTRS) +9%

Walgreens Boots Alliance (WBA) +9%

2. Consumer Staples Sector

Kraft Heinz (KHC) +8%

Campbell Soup (CPB) +8%

3. Industrial Sector

American Airlines (AAL) +8%

Delta Air Lines (DAL) +6%

3M Company (MMM) +6%

4. Financial Sector

U.S. Bancorp (USB) +6%

Top ETFs for the week

The following ETF themes worked well: low-volatility small caps, volatility, high yield stocks, food & beverage, airlines. The top ETFs for the week include:

iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) 2.6%

Invesco High Yield Equity Dividend Achievers ETF (PEY) 2.2%

First Trust Nasdaq Food & Beverage ETF (FTXG) 2.1%

U.S. Global Jets ETF (JETS) 2.0%

Will 3Q Earnings Steepen the Slide in Stocks?

* The third quarter earnings reporting season gains momentum this week. Several S&P 500 members from various industries are due to report. The reporting companies include Bank of America, International Business Machines, Johnson & Johnson, Procter & Gamble, Tesla, Union Pacific, and Verizon Communications.

* The latest updates on the state of the housing industry are due. The data include September housing starts, building permits, and existing home sales. Economists expect housing starts and existing home sales to decline in September from August; they expect building permits to stay flat.

* The Conference Board reports the Leading Economic Index for the U.S. Data on third-quarter gross domestic product growth in China and September inflation in the U.K. are due as well.

* Several Fed officials speak on Wednesday, Thursday, and Friday. Given the emphasis on inflation, investors will look for hints on the size of the future interest rate increases.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Last week, the S&P 500 gained 1.6% after swinging wildly in both directions. Investors tried to predict the impact of the economic data on Fed policy. Weakness in factory activity and fewer job openings spurred stocks to rally. The gains shrunk after the September jobs report. Wall Street awaits a big week that marks the start of the third quarter earnings reporting season. The economic calendar includes data on inflation and minutes from the Fed’s last interest rate policy meeting.

The S&P 500 swung by nearly 3%, up and down, on three of the five days last week as investors tried to assess the impact of economic data on interest rates.

Stocks started the week of October 3 with a bang as bond yields tumbled in response to weaker-than-expected manufacturing data and fewer job openings.

The Institute for Supply Management (ISM) reported that its manufacturing index fell to 50.9 in September, its lowest since May 2020. Economists surveyed by Dow Jones expected a reading of 52.0.

The Bureau of Labor Statistics reported a decline of over 1 million job openings in August to 10.1 million. The tally trailed FactSet’s estimate by 1 million.

A sizeable part of the gains in stock price reversed later in the week as comments from Federal Reserve officials and economic data raised interest rate worries.

The Presidents of Chicago, New York, and San Francisco Federal Reserve said inflation is troublesome. They insisted that the central bank would continue to raise interest rates to combat inflation.

Further, the ISM reported that its services index declined by a modest 0.2% in September to 56.7 after its employment component rose by 2.8%. Economists had expected the index to fall by 1.0% to 56.0.

The S&P 500 dropped 2.8% after the Labor Department released the September jobs report on Friday. The report showed the U.S. economy added 263,000 jobs in September, slightly below consensus economists’ estimate of 275,000. Yet, the unemployment rate fell to 3.5% from 3.7% in August. Average hourly earnings rose 0.3%.

Investors surmised Fed officials would raise interest rates aggressively to combat the support inflation is getting from continued growth in the number of jobs and wages.

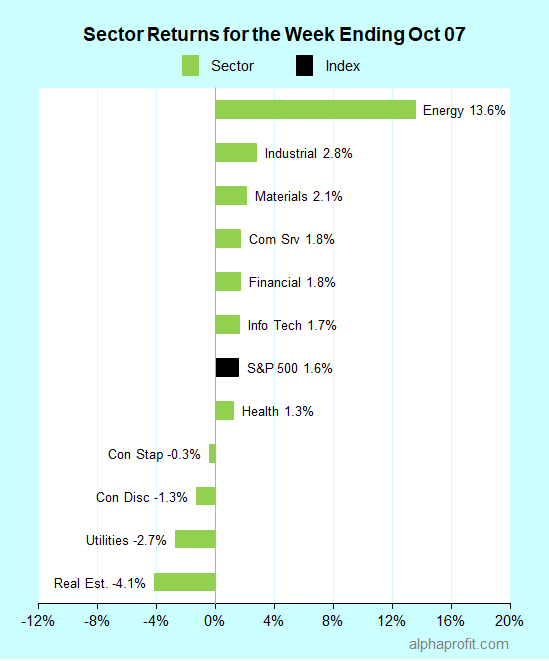

For the week ending October 07, the S&P 500 (SPY) rose 1.6%. Seven of the 11 sectors gained.

Energy (XLE) gained the most, while real estate (XLRE) lost the most.

Leading and lagging sectors for the week ending October 07, 2022.

The S&P 500’s top 10 winners included the following:

1. Health Care Sector

DexCom (DXC) +27% – The week’s top performer in the S&P 500.

2. Energy Sector

APA Corp. (APA) +24%

Marathon Oil (MRO) +24%

Halliburton (HAL) +24%

Devon Energy (DVN) +20%

Schlumberger (SLB) +19%

Pioneer Natural Resources (PXD) +19%

Diamondback Energy (FANG) +18%

Hess Corp. (HES) +18%

3. Consumer Discretionary Sector

Wynn Resorts (WYNN) +16%

Top ETFs for the week

The following ETF themes worked well: energy in various flavors including oil services, oil & gas exploration, oil, and natural gas. The top ETFs for the week include:

VanEck Oil Services ETF (OIH) 17.1%

United States Oil Fund, LP (USO) 15.0%

SPDR S&P Oil & Gas Exploration & Production ETF (XOP) 14.3%

First Trust Natural Gas ETF (FCG) 13.6%

Energy Select Sector SPDR Fund (XLE) 13.6%

Wall Street Awaits a Big Week Starting on October 10

* The third quarter earnings reporting season kicks off this week. Investors will focus on the earnings reports from the financial sector as several big names, including JPMorgan Chase, Morgan Stanley, BlackRock, and Citigroup, report this week. According to FactSet, analysts expect financial sector earnings to fall 13.5% this quarter. PepsiCo, Taiwan Semiconductor, Delta Air Lines, and UnitedHealth report outside the financial sector.

* Investors will have plenty of items to ponder about the state of the economy. Data on inflation & retail sales and the minutes from the Federal Reserve’s September 20-21 interest rate policy meeting are due. According to TradingEconomics.com, economists expect the consumer price index (CPI) to rise 0.2% in September, compared with a gain of 0.1% in August. They expect the increase in the CPI to moderate to 8.1% in September, from 8.3% in August. Economists expect core CPI inflation, which excludes food and energy prices, to show a 6.5% annual increase in September, up from 6.3% in August.

* A new wave of COVID cases appears to be gaining traction in Europe, where infections and hospitalizations are up. Two Omicron subvariants account for most of the new cases, while newer subvariants are gaining ground. With European economies already battered by the energy crisis, a further rise in COVID cases can become another cause of concern as colder weather moves in.

* The week is shaping up to be a big one for crypto finance. The G20 nations meet in Washington on Wednesday and Thursday. G20’s Financial Stability Board (FSB) will set out plans for regulating crypto markets and decentralized financial industries at this meeting. The regulations could make it harder for cryptocurrencies to expand their services without complying with regulations.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Economic data and comments from Federal Reserve officials intensified investors’ recession fears. Inflation exceeded expectations while the job market showed no sign of wilting. Fed officials reiterated their commitment to containing inflation, even at the expense of the economy. The economy and the Fed remain in focus this week. The Labor Department reports on job creation in September on Friday. Speeches from Fed officials could also move stock prices.

Investors became increasingly concerned that the Federal Reserve will aggressively raise interest rates in the coming months to combat inflation.

The personal consumption expenditure (PCE) price index, the Federal Reserve’s preferred inflation measure, showed that core consumer prices climbed by 0.6% in August, exceeding economists’ 0.5% forecast. The core PCE rose 4.9% year-over-year, higher than economists’ 4.7% forecast.

Jobless claims for the week ending September 24 exceeded consensus economists’ forecast. The Labor Department’s report showed initial claims for unemployment benefits fell by 16,000 to 193,000, the lowest since late April.

Investors also digested comments from several Federal Reserve officials who reiterated that the central bank would keep interest rates elevated to combat inflation and warned against prematurely easing interest rates.

The S&P Case-Shiller home price index provided some calm in an otherwise dismal week. The CSI showed higher interest rates are cooling the housing market. Prices across the nation fell at the fastest rate in the index’s history from June to July.

Meanwhile, inflation in the Eurozone set a new record high of 10% in September. The British currency fell to an all-time low against the dollar. The Bank of England said it would temporarily purchase long-dated UK government bonds in an effort to stabilize its plunging currency.

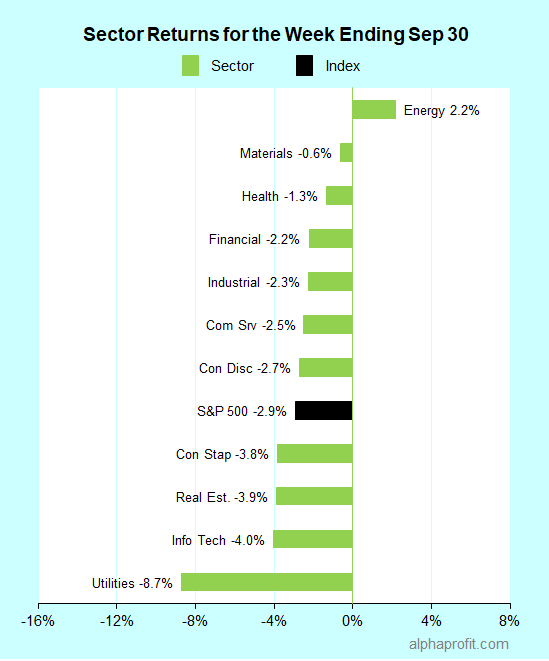

For the week ending September 30, the S&P 500 (SPY) fell 2.9%. Ten of the 11 sectors declined.

Energy (XLE) was the only sector to gain, while utilities (XLU) lost the most.

Leading and lagging sectors for the week ending September 30, 2022.

The S&P 500’s top 10 winners included the following:

1. Health Care Sector

Biogen (BIIB) +35% – The week’s top performer in the S&P 500.

Charles River Laboratories (CRL) +5%

2. Energy Sector

Marathon Petroleum (MPC) +9%

Valero Energy (VLO) +6%

Phillips 66 (PSX) +6%

Occidental Petroleum (OXY) +5%

Diamondback Energy (FANG) +5%

3. Consumer Discretionary Sector

Las Vegas Sands (LVS) +6%

Wynn Resorts (WYNN) +6%

4. Communication Services Sector

Twitter (TWTR) +5%

Top ETFs for the week

The following ETF themes worked well: precious metals, gold, silver, oil & gas, uranium, and biotechnology. The top ETFs for the week include:

ETFMG Prime Junior Silver Miners ETF (SILJ) 9.6%

VanEck Junior Gold Miners ETF (GDXJ) 9.1%

SPDR S&P Oil & Gas Exploration & Production ETF (XOP) 5.2%

Sprott Uranium Miners ETF (URNM) 3.9%

SPDR S&P Biotech ETF (XBI) 3.5%

Where are Stocks Headed after Falling 9% in September?

* The start of a new month brings fresh economic data, spearheaded by the September jobs report. The Labor Department’s report on Friday should show how well the labor market is holding up in the face of three 0.75% step-ups in benchmark interest rates. Economists surveyed by Dow Jones expect the economy to add 275,000 nonfarm jobs in September, down from August’s 315,000. They expect the unemployment rate to remain unchanged at 3.7%. Economists also expect modest declines in manufacturing and service activity measures from the Institute of Supply Management.

* The Federal Reserve Bank of Cleveland’s President, Mester, a member of the interest rate-setting Federal Open Market Committee, speaks on Tuesday and Thursday next week.

* A handful of consumer staples companies in the S&P 500 index report earnings. They include Conagra, Constellation Brands, Lamb Weston, and McCormick.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Sign up for the FREE investment newsletter AlphaProfit Money Matters and immediately receive Two Special Reports

Five Smart Ways to Profit from Sector Funds and ETFs

Avoid Three Common Mistakes ETF Investors Make

Don’t miss timely investment tips. Stay ahead of the market with AlphaProfit MoneyMatters in your inbox

Premium Service Performance

Model Portfolio Annualized Returns

DEC. 1993 to DEC. 2025

Fidelity Agg. Growth

17.6%

Fidelity Growth

14.6%

ETF Agg. Growth

17.4%

ETF Growth

14.4%

ETF Style Rot. (since 2009)

11.3%

S&P 500

10.8%

Stock Recommendation Returns

DEC. 2013 to DEC. 2025

Win Rate

91%

Avg. Holding Period

2.6 months

Avg. Gain

13.1%

MEET

DR. SAM SUBRAMANIAN

Sam Subramanian PhD, MBA has credentials that are the envy of most investment advisers. He combines strong quantitative skills with deep financial expertise and insights on inner workings of Wall Street and corporations. His creativity has helped him win 16 U. S. patents.

Prior to founding AlphaProfit Investments, LLC, Sam worked in positions of increasing responsibility in Finance and Corporate Strategy for McKinsey & Company, Exxon Corporation, and Unocal Corporation. His work centered on Acquisitions and Divestitures, Asset Valuation, Trading, Bankruptcies, and Risk Management.

Well aware of the dismal returns produced by money managers, he was determined to take charge of his own investments. He created a low cost, low effort but high return investing system and rigorously tested it for over two decades using his own money.

This high-performance system helped Sam to quickly become financially independent. Sam still invests his money, using the now award-winning system he created. He shares the unbiased, crystal-clear recommendations and market moves with his subscribers.