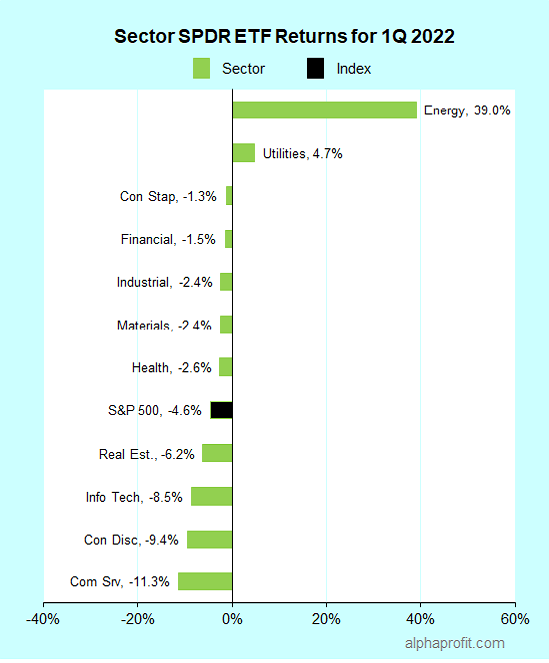

The S&P 500 fell 2.2% during the week, shortened by the Good Friday holiday. Bond yields continued their rise after inflation reports showed robust increases in consumer and producer prices. Investors also contended with mixed bank earnings and additional disruptions to exports from China.

Investors focused on inflation data and bond yields after consumer and producer price indexes rose sharply in March.

The CPI increased 8.5% in a year, the fastest annual gain since December 1981, while the PPI gained 11.2%, its highest yearly increase since 2010.

The yield on the 10-year Treasury bond added 0.12% for the week, ending at 2.83%.

In other economic data, retail sales rose a less-than-expected 0.5% in March as higher gasoline prices impacted household spending.

Banks kicked off the first-quarter earnings reporting season. Although the bottom line topped analysts’ estimates, the reports failed to enthuse investors. Banks reported a sharp decline in profits and warned of credit losses to rise in future quarters.

China expanded lockdowns beyond Shanghai to other cities in response to rising COVID cases. The Japanese bank Nomura estimates that 45 Chinese cities that account for nearly 40% of China’s economic output have implemented full or partial lockdowns.

News of supply chain disruptions from widespread lockdowns in China and rising bond yields hit technology stocks hard.

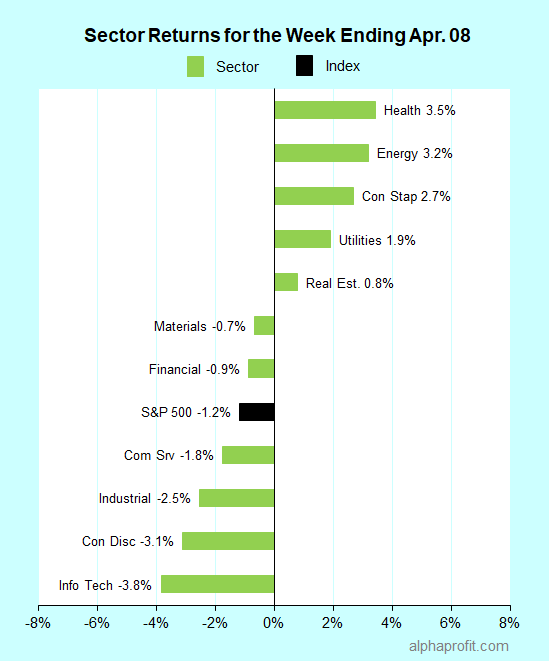

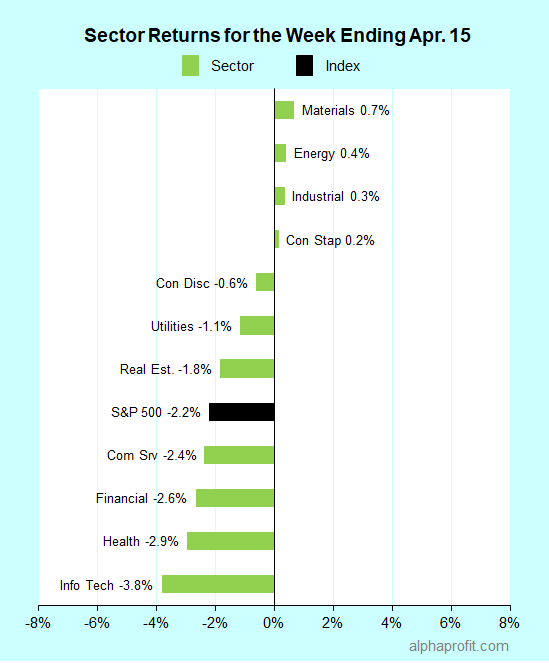

For the week ending April 15, the S&P 500 (SPY) fell 2.2%. Four of the 11 sectors advanced.

Leading and lagging sectors as 1Q22 earnings reports broaden beyond financials – April 15, 2022.

Materials (XLB), energy (XLE), and industrials (XLI) bucked the S&P 500, gaining 0.3% or more.

Information technology (XLK), health care (XLV), and financials (XLF) lagged the S&P 500.

The S&P 500’s top 10 winners included the following:

1. Consumer Discretionary Sector

- Bath & Body Works (BBWI) +15%

- PVH Corp. (PVH) +11%

- Marriott International (MAR) +10%

Delta Air Lines’ earnings outlook and the state of the travel industry boosted shares of hotel chain Marriott.

2. Industrials Sector

- Delta Air Lines (DAL) +14%

- American Airlines Group (AAL) +12%

- Southwest Airlines (LUV) +10%

Airline shares rallied broadly after Delta Air Lines reported lower losses than expected in the past quarter and forecasted profits in the current quarter due to historically high demand.

3. Consumer Staples Sector

- Molson Coors (TAP) +10%

4. Energy Sector

- Coterra Energy (CTRA) +10%

The natural gas producer rallied after JP Morgan and Wells Fargo raised their price targets on Coterra shares to imply an upside of over 25%.

5. Materials Sector

- Nucor Corp. (NUE) +10%

Nucor shares rallied ahead of the steelmaker reporting earnings this week on April 21.

6. Communication Services Sector

- DISH Network (DISH) +9%

Top ETFs for the week

The following ETFs themes worked well: airlines, metals & mining, commodities, gold, and silver. The top ETFs for the week include:

- U.S. Global Jets ETF (JETS) +8.0%

- SPDR S&P Metals and Mining ETF (XME) +7.3%

- Invesco Optimum Yield Div. Commodity Strategy ETF (PDBC) +5.4%

- VanEck Junior Gold Miners ETF (GDXJ) +5.4%

- ETFMG Prime Junior Silver Miners ETF (SILJ) +4.6%

Top Fidelity Fund for the week

- Fidelity Select Gold (FSAGX) +4.7%

Will 1Q22 Earnings Reports Perk Up Stocks?

The first-quarter earnings reporting season gathers some steam this week. Yet, earnings reports may not get the attention they usually do. Investors are likely to remain fixated on persistently high inflation, the Federal Reserve’s interest rate policy, and the war in Ukraine.

* Federal Reserve Chair Powell participates in a panel at the International Monetary Fund on Thursday to discuss the global economy. Powell’s comments may well be the highlight of the week.

* This week, the earnings reporting season broadens beyond financials to a mix of defensive and economically sensitive companies. The reporting companies include defensives like Johnson & Johnson, Procter & Gamble, and Verizon and economically sensitive ones like American Express, Tesla, and Union Pacific. Investors will focus on corporate earnings commentaries to understand the impact of inflation, rising commodity prices, and supply chain disruptions on profits.

* Investors are worried about housing demand due to the sharp increase in mortgage rates this year. The week’s economic reports should help investors gauge how the housing sector is doing. The economic calendar includes homebuilder sentiment, housing starts, and existing home sales data.

* The fallout from the war in Ukraine remains a concern for investors. The war has pushed up commodity prices, boosting inflation.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Sign up free to receive Looking Back, Looking Forward in your Inbox.

Learn more:

How AlphaProfit's investment strategy minimizes your risk

How AlphaProfit keeps your fees and expenses low

Performance of model portfolios & recommendations in AlphaProfit's Premium Service investment newsletter

AlphaProfit's free and premium investment newsletters