Stocks contributing to the performance of the above Fidelity funds likely include small-cap companies SiTime (SITM), Sprout Social (SPT), and TechTarget (TTGT). Among large-caps, American International Group (AIG), Alynylam Pharma (ALNY), Facebook(FB), Adobe (ADBE), Alphabet (GOOGL), and Bank of America (BAC) drove gains.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Wall Street rallied to push the S&P 500 index above 4,500 for the first time after Fed Chairman successfully avoided a taper tantrum. Powell said tapering of bond purchases is likely to begin this year while stressing tapering does not mean tightening. The nation’s top employers moved to mandate vaccinations for their employees after the U. S. FDA granted full approval for the Pfizer/BioNTech COVID-19 vaccine.

The past week was a good one for U. S. stocks. They rallied in the lead-up to Federal Reserve Chairman Powell’s speech at Jackson Hole, WY, on Friday. Investors bid up stock prices believing Powell would try to avoid a repeat of the 2013 taper tantrum. They viewed the central bank’s decision to hold the Jackson Hole event virtually as a signal the Fed sees a continued need to support the economy.

Chairman Powell did not disappoint investors. Powell said the Fed sees sufficient progress on inflation, but the labor market has not yet improved enough to start tapering monthly bond purchases. He added the Fed has “much ground to cover” to reach its goal of maximum employment. Powell emphasized that the tapering of bond purchases does not mean the central bank will automatically raise interest rates.

Economic data turned out as expected. The Commerce Department reported the personal consumption expenditures index rose 4.2% in the 12 months ending in July. While July marked the highest year-over-year increase in the PCE since 1991, the increase stemmed primarily from transitory factors. The University of Michigan’s consumer-sentiment index slipped as the spread of the coronavirus delta variant dented consumer optimism.

In other developments, the U. S. FDA granted full approval to the COVID-19 vaccine developed by Pfizer and BioNTech. Several of the nation’s leading employers moved to mandate vaccinations for at least some of their employees.

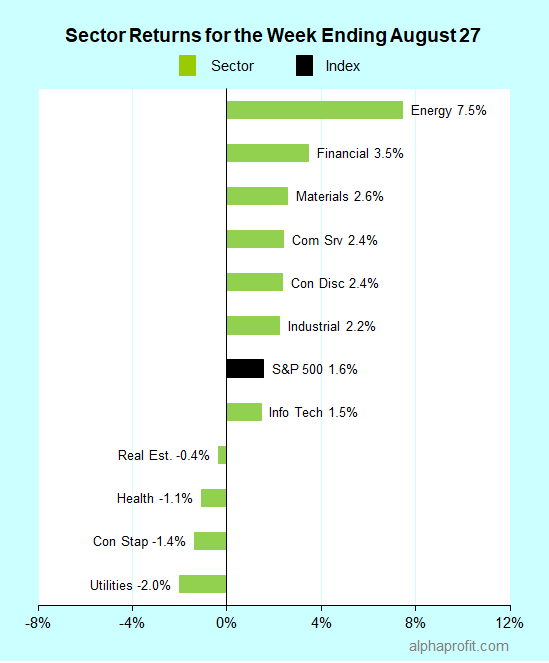

For the week ending August 27, the S&P 500 (SPY) rose 1.6%. Seven of the 11 sectors gained.

Leaders and laggards for the week ending August 27, 2021.

Energy (XLE), financials (XLF), and materials (XLB) led the benchmark gaining 2.6% or more.

Utilities (XLU), consumer staples (XLP), and health care (XLV) lagged the S&P 500.

Market breadth was positive. The number of advancing stocks in the S&P 500 led the number of decliners by a 5-to-2 ratio.

The S&P 500’s top 10 winners list included an even split of consumer discretionary and energy companies.

1. Consumer Discretionary

Online gambling companies and casino operators featured prominently among the week’s top 10 winners. Online gambling company Penn National Gaming (PENN) rose 24% to claim honors as the week’s top performer in the S&P 500. Casino operators Caesars Entertainment (CZR), Las Vegas Sands (LVS), Wynn Resorts (WYNN), and MGM Resorts International (MGM) also figured in the list after gaining 13-22% each.

Online gambling shares perked up on brightening prospects amidst the start of the college football and NFL seasons. Influential investor Cathy Wood sparked interest by increasing the stake of ARK ETFs in digital sports entertainment & gaming company DraftKings. The Wall Street Journal reported Disney’s ESPN unit is seeking to license its brand to DraftKings and casino operator Caesars Entertainment (CZR) for at least $3 billion over several years. Separately, Caesars Entertainment announced its first sports betting partnership with the Fiesta Bowl organization.

Las Vegas Sands, Wynn, and MGM with operations in Macau surged after Macau’s government relaxed COVID-testing rules for visitors from mainland China.

2. Energy

The S&P 500 top 10 winner list included five energy companies. Three of them were oil & gas producers Apache (APA), Devon Energy (DVN), and Occidental Petroleum (OXY); they each gained between 17% and 18%. Energy services companies Baker Hughes (BKR) and Halliburton (HAL) rose 13% each, claiming the other two spots.

Oil had its best week since June 2020, advancing 10%. Expectations of OPEC+ reining the increase in production at the upcoming September 1 meeting due to concerns with the delta variant drove the advance. Nearly 60% of U. S. Gulf Coast oil production shut down ahead of Hurricane Ida, limiting oil supplies. A decline in the U. S. dollar also supported the gain in oil.

Top ETFs for the week

The following ETFs themes worked well: oil & gas production, copper & gold miners, Chinese Internet, and cybersecurity. The top ETFs for the week include:

SPDR S&P Oil & Gas Exploration & Production ETF (XOP) +14.0%

The Labor Department reports August jobs data at the end of the week. The oil market will closely watch Hurricane Ida that appears to be heading towards Louisiana. Broadcom, Zoom Video, and a handful of consumer staples companies report earnings this week.

* Investor’s focal point moves to the August jobs report this week since Fed Chairman Powell has emphasized the need for more strong job creation before the central bank would start to unwind its bond purchases. The report should provide insights into the impact of the delta variant on the job market. Economists surveyed by Dow Jones expect the economy to have created 750,000 jobs in August, pushing the unemployment rate lower to 5.2% from 5.4% in July. For comparison purposes, the economy added 943,000 jobs in July.

* Petroleum product prices rallied last week, partly on curtailed U. S. Gulf Coast production. Oil & gas producers shut down nearly 60% of their Gulf of Mexico production ahead of Hurricane Ida. The U. S. weather service forecasts Ida to hit Louisiana, home to many refineries.

* Wall Street will get a read on the ongoing semiconductor chip shortage, inflation, and the delta variant’s impact on return-to-office via earnings reports. Semiconductor chip maker Broadcom, consumer staples companies Brown-Forman, Campbell Soup, & Hormel, and communication services provider Zoom Video report their earnings this week.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

U. S. stocks ended lower for the week as fears over the spread of the coronavirus delta variant sapped investor enthusiasm. The possibility of the Federal Reserve tapering bond purchases soon also weighed on stocks. Such fears eased after Fed Governor Kaplan’s comments on having an open mind about monetary policy.

A sharp rise in U. S. COVID cases, hospitalizations, and deaths dampened investor enthusiasm. The 7-day average of daily new U. S. cases hovered around 140,000, up from about 85,000 at the beginning of August.

Abroad, several Asian nations implemented drastic measures to curb the resurgence of COVID-19 from the highly contagious delta variant.

Worries of the impact of the delta variant on commodity demand weighed on prices. Oil was among the casualties, losing 9% for the week.

The minutes of the July 27-28 Federal Open Market Committee meeting also pressured stocks. They showed the Federal Reserve is willing to reduce monthly bond purchases in 2021.

Comments from Dallas Federal Reserve Governor Kaplan cheered investors on Friday. In an interview with Fox Business Network, Kaplan called the delta variant “the big imponderable” in the economic outlook. Kaplan also said the delta variant has caused him to have an open mind about the path of monetary policy.

The “Buy the Dip” group of investors resurfaced on Friday, pushing stock prices higher. Growth stocks were in favor as the yield on the 10-year Treasury bond ended the week 0.04% lower.

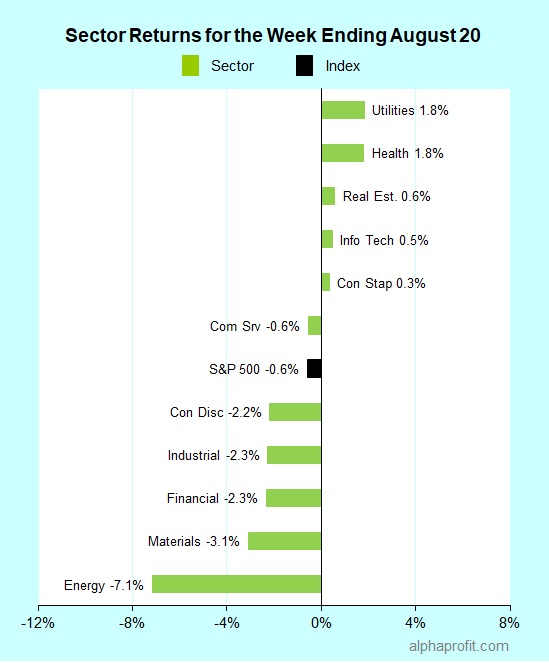

For the week ending August 20, the S&P 500 (SPY) fell 0.6%. Five of the 11 sectors gained.

Leaders and laggards for the week ending August 20, 2021.

Utilities (XLU), health care (XLV), and real estate (XLRE) bucked the S&P 500, gaining 0.6% or more.

Energy (XLE), materials (XLB), and financials (XLF) lagged the benchmark.

Market breadth was negative. The number of advancing stocks in the S&P 500 lagged the number of decliners by a 9-to-16 ratio.

The S&P 500’s top 10 winners included communication services, consumer discretionary, consumer staples, health care, industrial, information technology, and materials companies.

1. Consumer Staples

Kroger (KR) +10% – The grocery store chain rose 10% to claims honors as the week’s top performer in the S&P 500. The shares rallied after Warren Buffett’s Berkshire Hathaway disclosed buying 11 million Kroger shares, upping its stake in the supermarket to 8.3%.

2. Consumer Discretionary

Lowe’s (LOW) +9% – The builder materials retailer upped its full-year financial outlook, attributed the higher projections to the potential for margin expansion and market share gains. Lowe’s topped analysts’ second-quarter sales & EPS expectations, despite a 2.2% drop in same-store sales.

Bath & Body Works, Inc. (BBWI) +9% – The spinoff from L Brands reported earnings as an independent company for the first time. Bath & Body Works beat analysts’ quarterly EPS forecast by nearly 30% after sales rose 36% from the year-ago quarter.

3. Health Care

Abiomed (ABMD) +8% – The U. S. FDA designated Abiomed’s Impella ECP heart pump a breakthrough device, implying priority for the device’s regulatory review.

Regeneron Pharmaceuticals (REGN) +6% – The Medicines and Healthcare products Regulatory Agency in the U. K. approved Regeneron’s COVID antibody cocktail for use in patients. The Governors of Florida and Texas also recommended the drug for treating patients with COVID.

Other Top 10 Winners

The S&P 500’s top 10 winners for the week also included:

The following ETFs themes worked well: volatility futures, health care including medical devices & service providers, and utilities. The top ETFs for the week include:

iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) +5.6%

iShares U.S. Medical Devices ETF (IHI) +2.0%

iShares U.S. Healthcare Providers ETF (IHF) +2.0%

Utilities Select Sector SPDR Fund (XLU) +1.8%

Health Care Select Sector SPDR Fund (XLV) +1.8%

Top Fidelity Fund for the week

Fidelity Select Medical Technology and Devices (FSMEX) +2.0%

Looking ahead to the week of August 23

The Federal Reserve’s efforts to reverse its easy money policy will be a dominant theme for markets this week, as central bankers gather in Jackson Hole, Wyoming. Investors also get data on inflation and the housing industry. Salesforece.com and Workday are among the companies reporting earnings this week.

* Federal Reserve officials gather for their annual symposium at Jackson Hole, Wyoming. The Fed Chairman’s speech on Friday is typically the highlight of the meeting. Several past Fed chairs have used this speech to communicate messages related to interest rate policy. Investors await Chairman Powell’s comments on the economic recovery from COVID and the impact of the coronavirus delta variant. They are waiting to see if the delta variant could delay the Fed’s timetable for reducing $120 billion in monthly bond purchases.

* The economic calendar includes inflation and housing data. The Federal Reserve’s preferred inflation measure, the personal consumption expenditures data, and the inflation index are due on Friday. Briefing.com expects PCE to rise 0.4% from June to July, a tad less than 0.5% from May to June. Existing and new home sales are due on Monday and Tuesday, respectively.

* A handful of keenly watched earnings reports post this week. They include software firms salesforce.com & Workday, medical devices maker Medtronic, retailers Dollar General & Best Buy, and homebuilder Toll Brothers.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

U.S. stocks managed to grind to new highs in the face of rising COVID cases. The passage of the infrastructure bill in the Senate and data suggesting moderation in inflation boosted investor confidence. Consumer sentiment, however, succumbed to the resurgence in COVID cases. The reflation trade was in full flow. Value stocks such as materials and financials led the advance.

The U.S. Senate passed a $1 trillion infrastructure package with broad bipartisan support. The package includes billions of dollars for upgrading transportation infrastructure, broadband internet, electric grids, and more. This package now needs to be passed by the House and signed into law by President Biden.

Consumer price data showed the inflation rate moderating in July. The Labor Department reported the consumer price index rose 0.5% in July after climbing 0.9% in June. The drop in month-to-month inflation eased concerns of runaway inflation. Further, core inflation excluding food and energy prices rose by 0.3% in July, a tad below economists’ forecast.

The University of Michigan reported a sharp drop in its consumer-sentiment index. U. S. consumer sentiment fell from 81.2 in July to 70.2 in August, the lowest since December 2011. The university attributed the drop in sentiment to the rapid rise in the COVID cases, dashing hopes of an imminent end to the pandemic.

The 10-year Treasury yield stayed higher for most of the week after the Senate passed the infrastructure bill and inflation lagged forecasts. The 10-year yield slipped after consumer sentiment showed a steep drop and closed the week essentially where it started at 1.29%.

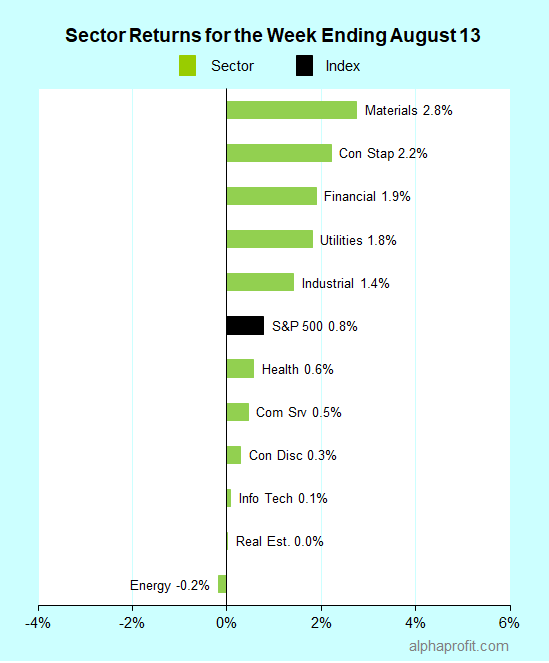

For the week ending August 13, the S&P 500 (SPY) rose 0.8%. Ten of the 11 sectors gained.

Leaders and laggards for the week ending August 13, 2021.

Materials (XLB), consumer staples (XLP), and financials (XLF) led the S&P 500, gaining 1.9% or more.

Energy (XLE), real estate (XLRE), and information technology (XLK) lagged the benchmark.

Market breadth was positive. The number of advancing stocks in the S&P 500 led the number of decliners by a 2-to-1 ratio.

The S&P 500’s top 10 winners included consumer discretionary, consumer staples, financial, health care, industrial, information technology, and materials companies.

1. Materials

Nucor Corp. (NUE) +20% – Shares of the steelmaker surged 20% to claims honors as the week’s top performer in the S&P 500. Investors bid Nucor shares higher after the Senate passed the $1 trillion infrastructure bill, bringing the legislation to increase spending on roads, bridges, and rail lines closer to reality. Nucor shares also got a lift from rising steel prices. The price of U. S. hot-rolled coil topped $1,900 per short ton, setting a new all-time high.

2. Health Care

Organon & Co. (OGN) +16% – The women’s health-focused spinoff from Merck reported earnings as an independent company for the first time. Organon beat analysts’ quarterly sales and EPS forecasts by 5% and 20%, respectively. The global healthcare company reaffirmed its full-year guidance and initiated a $0.28 a share quarterly dividend translating to a 3.2% yield.

Pfizer (PFE) +8% – Pfizer rallied as a member of the COVID vaccine makers group. The number of COVID cases continued to rise in the U. S. The FDA approved booster shots for immunocompromised individuals. Pfizer and Germany’s BioNTech (BNTX) are partners in the effort to develop & produce Comirnaty, an mRNA-based COVID vaccine.

3. Consumer Staples

Tyson Foods (TSN) +15% – The meat processor’s quarterly sales and EPS exceeded analysts’ forecasts by 8% and 62%, respectively. Tyson raised its full-year sales forecast, citing higher beef demand from restaurant re-openings.

Sysco Corp. (SYY) +7% – The food distributor swung to a profit from its prior-year loss as sales surged 82% from 2020’s COVID-impacted quarter. Sysco’s sales and EPS topped analysts’ forecasts. Citing robust July sales, Sysco raised its fiscal 2022 EPS guidance by 3%.

Other Top 10 Winners

The S&P 500’s top 10 winners for the week also included:

eCommerce marketplace operator eBay Inc. (EBAY) +13%

Online arts & crafts retailer Etsy, Inc. (ETSY) +8%

Railroad Kansas City Southern (KSU) +8%

Diversified insurer American International Group (AIG)+7%

Top ETFs for the week

The following ETFs themes worked well: metals including platinum & copper, infrastructure spending, and robotics. The top ETFs for the week include:

SPDR S&P Metals and Mining ETF (XME) +5.4%

Aberdeen Standard Physical Platinum Shares ETF (PPLT) +4.9%

Global X U.S. Infrastructure Development ETF (PAVE) +3.6%

Global X Robotics & Artificial Intelligence ETF (BOTZ) +3.1%

Global X Copper Miners ETF (COPX) +3.1%

Top Fidelity Fund for the week

Fidelity Agricultural Productivity (FARMX) +3.4%

Looking ahead to the week of August 16

Investors will look to the retail sector for insights on consumer health after consumer sentiment declined abruptly last week. The minutes of the July FOMC meeting can also be a market driver if it sheds light on the Fed’s tapering process. Investors are eyeing value stocks to see if they can extend their market leadership from the past week.

* Investors will look to economic data and retail sector earnings reports to assess the impact of the decline in consumer sentiment on consumer behavior. The Census Bureau releases the July retail sales report on Tuesday, with Dow Jones calling for a 0.2% decline. The week also includes earnings reports from several retailers, including Walmart, Home Depot, Lowe’s, Target, and Macy’s.

* The Federal Reserve releases the minutes of the July 27-28 FOMC meeting on Wednesday. Investors will scrutinize them for clues on the central bank’s plans to end its bond-buying program, also called the tapering process.

* Investors are watching if cyclical stocks can sustain their leadership from last week. While a rise in bond yields and a decline in COVID cases will support value stocks, economic data such as weekly jobless claims, industrial production, and the Empire State Manufacturing Index can likely play a role in sustaining the reflation trade.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Record-breaking upside surprises in the second-quarter earnings reports and the stronger-than-expected July jobs report boosted investors’ confidence in the economy. The number of daily new COVID cases rose seven-fold in July. Stocks closed the week at record highs, while the yield on the 10-year Treasury bond nudged higher.

Corporate America’s impressive stretch of second-quarter earnings reports continued. Of the nearly 450 of the S&P 500 members reporting earnings this quarter, 87% have topped earnings expectations. According to FactSet, the second quarter is on track to be best for earnings surprises since at least 2008.

The Labor Department reported the economy added 943,000 nonfarm jobs in July compared to economists’ 845,000 forecast. Job creation in July rose 5,000 from the June tally. The unemployment rate fell from 5.9% in June to 5.4% in July, marking a 16-month low. Wage inflation showed a 4% increase over the past year.

The jobs report soothed concerns of the economy faltering from the renewed surge in COVID casts. The 10-year Treasury yield turned around to close the week at 1.29%, after hitting a low of 1.13% earlier in the week.

On the public health front, mask mandates reappeared as the 7-day average of daily new COVID cases surged past 100,000 a day, up from 13,000 at the beginning of July.

The U. S. Senate introduced a bipartisan infrastructure bill. The $1 trillion plan includes investments in roads, high-speed internet, and other infrastructure.

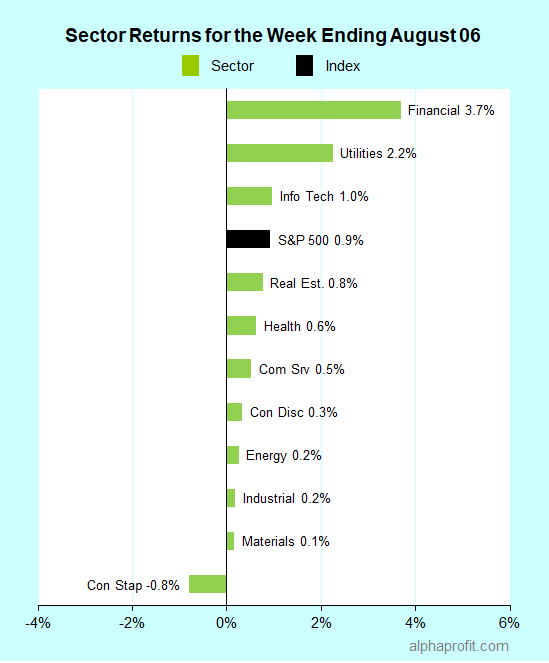

For the week ending August 6, the S&P 500 (SPY) rose 0.9%. Ten of the 11 sectors gained.

Leaders and laggards for the week ending August 06, 2021.

Financials (XLF), utilities (XLU), and information technology (XLK) led the S&P 500, gaining 1.0% or more.

Consumer staples (XLP), materials, and industrials (XLI) lagged the benchmark.

Market breadth was positive. The number of advancing stocks in the S&P 500 led the number of decliners by a 2-to-1 ratio.

Consumer discretionary, health care, and information technology companies accounted for eight of the S&P 500’s top 10 winners. Lithium producer Albemarle (ALB) and insurer Lincoln National (LNC) rounded out the top 10.

1. Consumer Discretionary

Under Armour (UAA) +22% – Shares of the apparel company rocketed 22% to claims honors as the week’s top performer in the S&P 500. Under Armour topped analysts’ second-quarter sales forecast by 11% and earned 24 cents a share compared to analysts’ 6 cents a share estimate. Under Armour also raised full-year sales and EPS guidance. n.

Hanesbrands (HBI) and Ralph Lauren (RL) +9% each – Shares of both apparel makers rose high single-digits after topping analysts’ quarterly sales and EPS forecasts.

2. Health Care

Moderna (MRNA) +17% – The COVID vaccine maker blew past analysts’ second-quarter sales and EPS estimates. The biotechnology company has already secured 2022 supply deals totaling $12 billion with options for another $8 billion sales. Moderna also announced its respiratory syncytial virus vaccine candidate received fast track designation from the U. S. FDA.

DaVita (DVA) +11% – The dialysis services provider topped analysts’ EPS forecast for the second quarter after widening the operating margin by 2.3% to 22.4%. DaVita also raised the mid-point of its full-year EPS guidance by 6% to $9.10 a share.

3. Information Technology

Paycom Software (PAYC) +17% – The cloud-based human resource software provider earned $0.97 a share in the second quarter, $0.14 above analysts’ forecast. Paycom bumped up its full-year sales guidance by 2%.

Fortinet (FTNT) +12% – The cybersecurity solution provider rose after UBS raised Fortinet’s share price target and Jefferies raised Fortinet’s stock rating.

Gartner (IT) +11% – The information technology market research and consulting company raised its full-year sales and EPS guidance to imply growth of 11% and 55%, respectively, after topping analysts’ second-quarter sales and EPS estimates.

Top ETFs for the week

The following ETFs themes worked well: blockchain, carbon credit, banking, semiconductor, and biotechnology. The top ETFs for the week include:

Amplify Transformational Data Sharing ETF (BLOK) +9.2%

KraneShares Global Carbon ETF (KRBN) +5.0%

SPDR S&P Regional Banking ETF (KRE) +5.0%

SPDR S&P Semiconductor ETF (XSD) +3.9%

iShares Biotechnology ETF (IBB) +3.8%

Top Fidelity Fund for the week

Fidelity Select Banking (FSRBX) +4.4%

Looking ahead to the week of August 09

This week is a big one for inflation and economic data. The economic calendar includes readings on inflation at the consumer and producer levels as well as consumer sentiment. The week also includes speeches from a few Federal Reserve officials. The Treasury auctions nearly $125 billion in notes and bonds this week.

* Investors will focus their attention on inflation this week after Following a better-than-expected July jobs report. The consumer price index and the producer price index come out on Wednesday and Thursday, respectively. The consumer sentiment follows on Friday. Economists polled by Dow Jones expect the core consumer price index to show a 4.3% year over year in July, a tad slower than the 4.5% rise recorded in June.

* A few Federal Reserve officials speak in the week ahead. Investors will look to their comments to help clarify the central bank’s intentions on tapering bond purchases.

* The U. S. Treasury auctions nearly $125 billion in 3-year, 10-year, and 30-year Treasuries combined. The U. S. Senate may vote on the infrastructure bill.

* Second-quarter earnings reports slow to a trickle from last week’s breakneck pace. Disney, BioNTech, Baidu, eBay, and Barrick Gold are among the companies reporting.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

* iShares Residential and Multisector Real Estate ETF, REZ +8.1%

* Invesco S&P Global Water Index ETF, CGW +6.6%

* Invesco Water Resources ETF, PHO +6.1%

Stocks contributing to the performance of the above ETFs likely include China Northern Rare Earth Group High-Tech (SSE: 600111), Ganfeng Lithium (GNENF), Albemarle (ALB), Waters Corp. (WAT), Danaher (DHR), American Water Works (AWK), Equity Residential (EQR), and AvalonBay Communities (AVB).

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Fidelity funds focusing on water, medical technology & devices, real estate, and the Nordic region were top performers in July. Water stocks rose from optimism on the Infrastructure bill becoming law.

Top Fidelity Funds for July 2021

Excludes closed funds

* Fidelity Water Sustainability Fund, FLOWX +7.3%

* Fidelity Select Medical Technology and Devices Portfolio, FSMEX +6.1%

* Fidelity Real Estate Investment Portfolio, FRESX +5.1%

* Fidelity Real Estate Index Fund, FSRNX +4.4%

* Fidelity Nordic Fund, FNORX +4.4%

Stocks contributing to the performance of the above Fidelity funds likely include Danaher (DHR), Novo Nordisk A/S (NVO), American Water Works (AWK), Pentair PLC (PNR), Prologis (PLD), and Thermo Fisher Scientific (TMO).

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks closed the week at record highs after a surge in COVID cases from the delta variant threatened to extend the prior week’s decline. Stocks rallied for four straight days as investors bought on the dip. Analysts boosted second-quarter EPS forecasts for companies reporting later in the season, boosting investors’ appetite for stocks.

Stocks staged a turnaround after a renewed surge in COVID cases from the delta variant escalated worries of lockdowns returning to impact the economy. The Dow Jones Industrial Average slumped over 725 points on Monday, its highest one-day decline since October.

Upbeat earnings reports helped stocks to rebound. Investors bought on the dip as 88% of S&P 500 companies reporting earnings topped analysts’ second-quarter EPS forecasts.

The reports showed companies sustaining profit margins in the face of rising inflation. The profit margin for the reporting companies is averaging 12.8%, above the historic range, according to S&P Global.

The early trend in second-quarter earnings reports prompted analysts to raise EPS forecasts for companies to follow. According to FactSet, analysts now expect S&P 500 company earnings to grow 74% year-over-year in the second quarter, up from 63% they forecasted on June 30.

Stocks rose four straight days on the back of robust earnings reports to close the week at record highs. The DJIA scaled above 35,000 for the first time. Investors favored growth stocks over value stocks amidst the backdrop of rising COVID cases and falling bond yields.

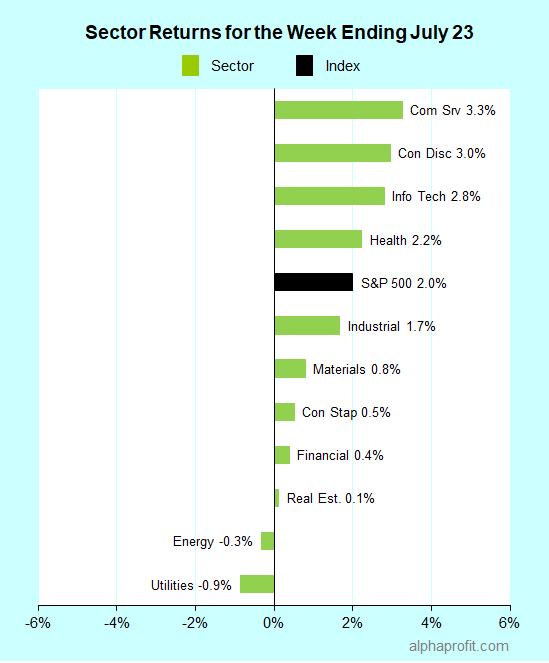

For the week ending July 23, the S&P 500 (SPY) rose 2.0%. Nine of the 11 sectors gained.

Leaders and laggards for the week ending July 23, 2021.

Communication services (XLC), consumer discretionary (XLY), and information technology (XLK) led the S&P 500, gaining 2.8% or more.

Utilities (XLU), energy (XLE), and real estate (XLRE) lagged the benchmark.

Market breadth was positive. The number of advancing stocks in the S&P 500 led the number of decliners by a 5-to-2 ratio.

Information technology and consumer discretionary companies accounted for seven of the S&P 500’s top 10 winners. Health care and communication services companies rounded out the top 10.

1. Health Care

Moderna (MRNA) +22% – Shares of the new entrant to the S&P 500 surged 22% to claim honors as the week’s top performer in the benchmark. Investors saw Moderna having more opportunities to increase COVID vaccine sales from rising concerns of the coronavirus delta variant. Moderna also announced new deals to supply its COVID vaccine to Japan and Taiwan.

HCA Healthcare (HCA) +13% – The hospital operator beat analysts’ second-quarter sales and EPS forecasts and raised full-year sales and EPS guidance.

2. Consumer Discretionary

Chipotle Mexican Grill (CMG) +17% – The burrito specialist’s results confirmed the changes it made in response to the pandemic work in a post-pandemic world. Chipotle’s second-quarter same-store sales surged 31% and 18% from the second quarter in 2020 and 2019, respectively. Chipotle expects this momentum to continue in the third quarter, with same-store sales growing 19-25% from the 2019 level.

Online marketplace Etsy Inc. (ETSY) and restaurant chain Domino’s Pizza (DPZ) were among the week’s top 10 winners, gaining 13% and 9%, respectively.

3. Communication Services

The Interpublic Group of Companies (IPG) +12% – The global advertising and marketing services company posted a 23% increase in sales in the second quarter that helped EPS top analysts forecasts by 63%. IPG also raised its full-year guidance for organic revenue growth to a range of 9-10%.

4. Information Technology

KLA Corp. (KLAC) and Lam Research (LRCX) +9% – Shares of semiconductor equipment companies rose as they benefit from semiconductor contract manufacturers, increasing production in response to semiconductor chip shortage.

Enphase Energy (ENPH) +9% – Shares of the solar energy storage system and technology company rose after JPMorgan increased its price target by $28 to $238 a share. Enphase reports second-quarter earnings on July 27.

Software company PTC Inc. (PTC) rose 9%, becoming the fourth information technology in the week’s top 10 winners.

Top ETFs for the week

The following ETFs themes worked well: rare earth, social media, cloud computing, home builders, health care. The top ETFs for the week include:

First Trust U. S. Equity Opportunities ETF (FPX) +6.6%

iShares U. S. Home Construction ETF (ITB) +5.9%

Invesco DWA Healthcare Momentum ETF (PTH) +5.9%

Top Fidelity Fund for the week

Fidelity Select Semiconductors (FSELX) +5.1%

Looking ahead to the week of July 26

The week includes several events with market-moving potential. First, the second-quarter earnings season is in its busiest week. Second, the FOMC meets to discuss monetary policy. Last, investors get a read on second-quarter GDP growth and June inflation.

* The Federal Open Market Committee meets on Tuesday and Wednesday to discuss interest rate policy. Economists expect the FOMC to leave interest rates unchanged. Investors are focusing on what Chairman Powell says about the coronavirus’ delta variant impact and risks. Investors will also be looking for clues on when the central bank may begin tapering its bond purchases.

* Nearly 170 S&P 500 members report second-quarter earnings this week, the busiest one of the reporting season. Index heavyweights Apple, Microsoft, Amazon, Alphabet, and Facebook report. The earnings calendar also includes reports from sector heavyweights Visa, Procter & Gamble, ExxonMobil, Pfizer, and United Parcel Service.

* The Commerce Department reports its GDP growth estimate for the second quarter. According to Briefing.com, economists expect the GDP to grow at an 8.5% annualized rate in the second quarter, marking the peak for growth. Wall Street also gets to look at inflation from the June reading for personal consumption expenditures, the Fed’s preferred measure. Investors will also be watching developments on the U. S. federal debt ceiling since the 2019 agreement to suspend the debt limit expires on August 1.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks pulled back from record highs to end their winning streak after three weeks. The nationwide count of daily new COVID cases rose from the delta variant of the coronavirus. Investors provided a muted response to second-quarter earnings reports. The surprising drop in consumer sentiment weighed heavily on stocks.

The delta variant of the coronavirus impacted stocks after public health officials said U. S. COVID cases are up 70% from the previous week. Several counties in California including, Los Angeles, and parts of Nevada, including Las Vegas, asked people to wear masks regardless of their vaccination status.

The S&P 500 companies reporting second-quarter earnings showed robust year-over-year growth. Over 85% of the reporting members beat analysts’ EPS forecasts. Several financial firms including, Citigroup, Goldman Sachs, PNC Financial, and Wells Fargo, topped analysts’ EPS forecast by over 40% each.

Investors were, however, not enthused. Stocks of reporting companies fell more often than they gained. The median decline of S&P 500 member reporting earnings last week amounted to 1.9%. Investors fretted over the impact of the resurgence in COVID cases on third-quarter earnings.

In economic data, U. S. retail sales rose 0.6% in June from May as consumers spent more on services and in-store goods. Economists expected retail sales to fall by 0.4%.

Inflation concerns lurked in the background through the week after the consumer price index rose 5.4% for the 12 months ending in June. Federal Reserve Chairman Powell told Congress the rise in inflation would likely be temporary. Investors perceived the surprising decline in consumer sentiment as the verdict on inflation for the week.

Stocks sold off after the University of Michigan’s consumer sentiment index fell to 80.8 in July from 85.5 in June, compared to economists’ forecast for the index to rise to 86.3. Investors interpreted the data as evidence for inflation concerns outweighing positive job growth trends. The survey showed consumers expecting the cost of living to rise 4.8% this year, the highest since 2008.

The yield on the 10-year Treasury note fell over 0.05% last week to close at 1.30%.

For the week ending July 16, the S&P 500 (SPY) fell 1.0%. Eight of the 11 sectors declined.

Leaders and laggards for the week ending July 16, 2021.

Utilities (XLU), consumer staples (XLP), and real estate (XLRE) bucked the S&P 500, gaining 0.7% or more.

Energy (XLE), consumer discretionary (XLY), and materials (XLB) lagged the benchmark.

Market breadth was negative. The number of declining stocks in the S&P 500 led the number of advancers by more than a 2-to-1 ratio.

Utility companies accounted for six of the S&P 500’s top 10 winners. Consumer staples, financial, and real estate companies rounded out the top 10.

1. Utilities

Eversource Energy (ES), Evergy (EVRG), Duke Energy (DUK), WEC Energy (WEC), NextEra Energy (NEE), and Ameren Corp. (AEE) +4 to 6% each – The defensive attributes of utility stocks and their 3.25% average dividend yield appealed to investors amidst falling bond yields and declining stock prices.

In company-specific news, Duke Energy hiked its quarterly dividend by 2%. Credit Suisse assumed coverage of NextEra Energy with an Outperform rating and $85 price target, implying a 9% upside.

2. Consumer Staples

PepsiCo (PEP) +4% – The beverage and snack giant topped analysts’ second-quarter sales and EPS forecasts by 7% and 12%, respectively, and provided an upbeat assessment for the remainder of 2021.

3. Financial

Visa (V) and Mastercard (MA) +4% each – Credit card networks fared well, with Visa setting a new all-time high and Mastercard approaching its all-time high set in April. India’s fifth-largest credit card issuer RBL Bank teamed up with Visa to issue credit cards. MasterCard announced a partnership with Verizon Communications to jointly develop contactless payments and new shopping formats.

4. Real Estate

Welltower (WELL) +4% – Health care REIT rose after RBC Capital Markets raised Welltower’s per-share funds from operations estimate for 2021, 2022, and 2023, citing stronger-than-expected improvement in senior housing occupancy rates from COVID.

Top ETFs for the week

The following ETFs themes worked well: agricultural commodities, utilities, Brazilian stocks, and residential real estate. The top ETFs for the week include:

Invesco DB Agriculture Fund (DBA) +3.7%

First Trust Global Tactical Commodity Strategy (FTGC) +2.7%

Utilities Select Sector SPDR Fund (XLU) +2.6%

iShares MSCI Brazil ETF (EWZ) +1.7%

iShares Residential and Multisector Real Estate (REZ) +1.7%

Top Fidelity Fund for the week

Fidelity Select Utilities (FSUTX) +1.2%

Looking ahead to the week of July 19

Earnings reports take center stage this week. Concerns about the delta variant of the coronavirus are rising. Falling long-term bond yields will continue to be among investor’s focal points, with the European Central Bank and the People’s Bank of China announcing interest rate decisions. The economic calendar includes data from the housing industry.

* The flow of second-quarter earnings picks up. Nearly 70 S&P 500 members report bringing the healthcare, communication services, information technology, and industrials sectors into focus. Sector heavyweights Johnson & Johnson, Netflix, Intel, and Honeywell, report this week. American Express, Coca-Cola, and NextEra Energy are among the other S&P 500 members reporting earnings this week.

* Investors are becoming antsy over the uptick in the daily number of new COVID cases from the delta variant. The 7-day daily new case average has risen to about 30,000, after bottoming in the latter part of June at around 12,000. Further increases in the number of cases can overshadow earnings reports and negatively impact stocks.

* Wall Street will maintain its focus on interest rates. The slide in yields suggests bond investors are unsure of the prospects of continued economic growth. The European Central Bank meets to discuss interest rate policy this week. With the recovery of the Eurozone economies stalled and COVID cases on the rise, the ECB could strengthen its commitment to low-interest rates and asset purchases. Investors also await the People Bank of China’s interest rate decision after the bank changed course abruptly last week, increasing liquidity.

* Several data points from the housing industry are due this week. They include housing starts, building permits, and existing home sales. Investors will look to assess the impact of falling lumber prices and mortgage rates on the housing industry.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Investor sentiment shifted dramatically during the short trading week. Investors grappled with worries of a global economic slowdown as inflation concerns gave way.

Investors swapped fears of runaway inflation with worries of a rapid slowdown in global economic growth during the holiday-shortened trading week.

Worries rose on the highly contagious COVID delta variant, pegging back the global economic rebound. Japan declared a state of emergency in Tokyo to curb the spread of coronavirus. The Olympics organizers responded by banning spectators at the Tokyo summer games scheduled from July 23 to August 8.

Economic data also sparked concerns about the strength of the U. S. economy. The Institute of Supply Management’s services activity measure fell to 60.1 in June from its May record, exceeding economists’ forecast. Weekly unemployment claims unexpectedly rose by 2,000 compared to economists forecast for a 20,000 decline.

Minutes of the Federal Open Market Committee’s June 15-16 meeting suggested officials may not be ready yet to tighten monetary policy.

After starting the week at 1.43%, the yield on the 10-year Treasury bond fell as low as 1.27% as worries of a global economic slowdown gripped investors.

A ‘buy the dip’ mentality pervaded the stock market on Friday. The resulting rally enabled the broad U. S. stock indexes to reverse earlier losses and end above the flat-line for the week.

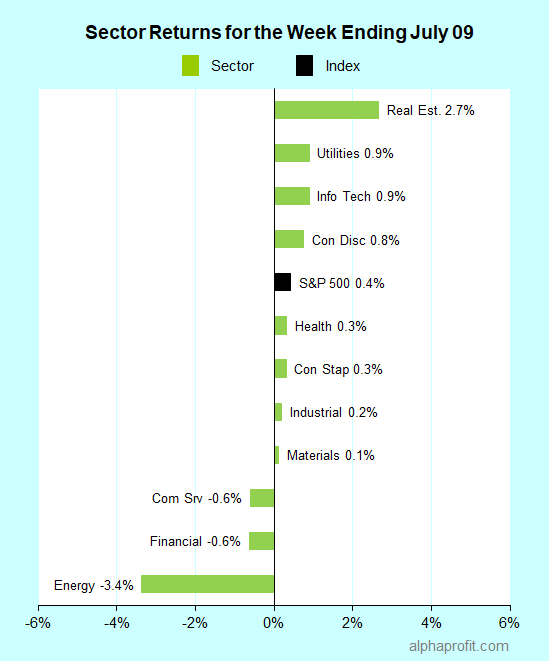

For the week ending July 9, the S&P 500 (SPY) rose 0.4%. Eight of the 11 sectors gained.

Leaders and laggards for the week ending July 09, 2021.

Real estate (XLRE), utilities (XLU), and information technology (XLK) led the S&P 500, gaining 0.9% or more.

Energy (XLE), financials (XLF), and communication services (XLC) lagged the benchmark.

Market breadth was barely positive. The number of advancing stocks in the S&P 500 led the number of decliners by a modest 14-to-11 ratio.

Information technology, consumer discretionary, and real estate companies collectively accounted for nine of the S&P 500’s top 10 winners. The winner list also included one industrial company in Generac (GNRC).

1. Information Technology

Oracle (ORCL) +7% – The enterprise software company was the week’s top performer in the S&P 500. Oracle shares surged on speculation the company may win a part of the Defense Department’s new cloud computing contract after the DoD canceled the $10 billion cloud computing contract previously awarded to Microsoft. Oracle (ORCL) and Amazon.com (AMZN) had challenged the award in court.

2. Consumer Discretionary

Amazon.com (AMZN) +6% – The company entered into a content deal with Comcast allowing Amazon’s streaming video services Prime Video and IMDb TV to carry content from Hollywood heavyweight Universal. Investors also warmed up to the possibility of Amazon’s web services unit getting a piece of the DoD’s new cloud computing contract.

3. Real Estate

Real Estate Investment Trusts (REITs) accounted for seven of the top 10 winners. Apartment owners Mid-America Apartment Communities (MAA), Essex Property Trust (ESS), and AvalonBay Communities (AVB) rose 5-6% each after RBC Capital Markets upped the price targets citing lower capitalization rates and higher funds from operations. Apartment REITs UDR, Inc. (UDR) and Equity Residential (EQR) joined the rally, gaining 4-5% each.

Timberland owner Weyerhaeuser (WY) and industrial properties owner Duke Realty (DRE) also featured among the top winners, rising 4% each.

Top ETFs for the week

The following ETFs themes worked well: rare earths, lithium & batteries, online retail, cybersecurity, and REITs. The top ETFs for the week include:

There is plenty for investors to look forward to this week. The second-quarter earnings reporting season kicks off amidst expectations for high year-over-year earnings growth. The economic calendar is also busy with investors getting a look at both inflation and growth measures.

* The second-quarter earnings report season kicks off this week. Analysts expect S&P 500 to grow EPS 64% year-over-year on average, the highest on record since the fourth quarter of 2009. The focus is on financials this week with JPMorgan Chase, Bank of America, Wells Fargo, Morgan Stanley, Citigroup, and Goldman Sachs reporting. The earnings calendar includes reports from non-financial firms such as UnitedHealth, PepsiCo, Delta Air Lines, and Alcoa.

* Investors will get a read on inflation this week. The June consumer price index (CPI) comes out on Tuesday. According to Briefing.com, economists’ consensus estimate sees the total CPI increasing 0.5% in June, a tad slower than 0.6% in May. The producer price index (PPI) follows the CPI on Wednesday. The PPI provides a perspective on inflation in wholesale prices.

* As for growth indicators, the Commerce Department’s Census Bureau reports June retail sales on Friday. Economists expect the decline in retail sales to moderate to 0.6% in June from 1.3% in May. Investors will also focus on the number of initial unemployment claim filings after they unexpectedly rose last week. Economists expect claims to decline by 13,000.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Sign up for the FREE investment newsletter AlphaProfit Money Matters and immediately receive Two Special Reports

Five Smart Ways to Profit from Sector Funds and ETFs

Avoid Three Common Mistakes ETF Investors Make

Don’t miss timely investment tips. Stay ahead of the market with AlphaProfit MoneyMatters in your inbox

Premium Service Performance

Model Portfolio Annualized Returns

DEC. 1993 to DEC. 2025

Fidelity Agg. Growth

17.6%

Fidelity Growth

14.6%

ETF Agg. Growth

17.4%

ETF Growth

14.4%

ETF Style Rot. (since 2009)

11.3%

S&P 500

10.8%

Stock Recommendation Returns

DEC. 2013 to DEC. 2025

Win Rate

91%

Avg. Holding Period

2.6 months

Avg. Gain

13.1%

MEET

DR. SAM SUBRAMANIAN

Sam Subramanian PhD, MBA has credentials that are the envy of most investment advisers. He combines strong quantitative skills with deep financial expertise and insights on inner workings of Wall Street and corporations. His creativity has helped him win 16 U. S. patents.

Prior to founding AlphaProfit Investments, LLC, Sam worked in positions of increasing responsibility in Finance and Corporate Strategy for McKinsey & Company, Exxon Corporation, and Unocal Corporation. His work centered on Acquisitions and Divestitures, Asset Valuation, Trading, Bankruptcies, and Risk Management.

Well aware of the dismal returns produced by money managers, he was determined to take charge of his own investments. He created a low cost, low effort but high return investing system and rigorously tested it for over two decades using his own money.

This high-performance system helped Sam to quickly become financially independent. Sam still invests his money, using the now award-winning system he created. He shares the unbiased, crystal-clear recommendations and market moves with his subscribers.