Atlanta Fed President Bostic’s comment favoring interest rate increases in 0.25% increments boosted market sentiment last week. Stocks rallied as the yield on the 10-year Treasury note dipped below the psychologically important 4.0% mark. This week, investors will focus on the jobs data and Fed Chair Powell’s Congressional testimony.

Investors digested comments from several Fed officials last week. Comments from Atlanta Federal Reserve President Raphael Bostic boosted market sentiment.

Bostic said the central bank should limit its interest rate hikes to 0.25% rather than pursue the 0.50% increase favored by other Fed officials.

With the effects of higher interest rates unlikely to be felt until spring, Bostic said a “slow and steady” course of action is appropriate since it would minimize the risk of starting a recession.

In economic data, the Institute for Supply Management (ISM) said its service activity index held steady at 55.1% in February, suggesting expansion. Economists polled by Dow Jones expected the index to fall to 54.3% from 55.2% in January. Encouragingly, the inflation measure in the service activity index fell by 2.2%.

Earlier, the ISM’s factory index remained below 50.0% at 47.7%, as predicted by economists. The inflation measure in the factory index spooked investors, rising by 6.8%.

China’s National Bureau of Statistics said its official manufacturing Purchasing Manager’s Index (PMI) increased to 52.6 in February, suggesting the re-opening of China’s economy from COVID restrictions is proceeding without setbacks. The February PMI reading marked the highest since April 2012.

The yield on the benchmark 10-year Treasury note dipped below the 4.0% threshold after Bostic’s comment to close the week at 3.97%.

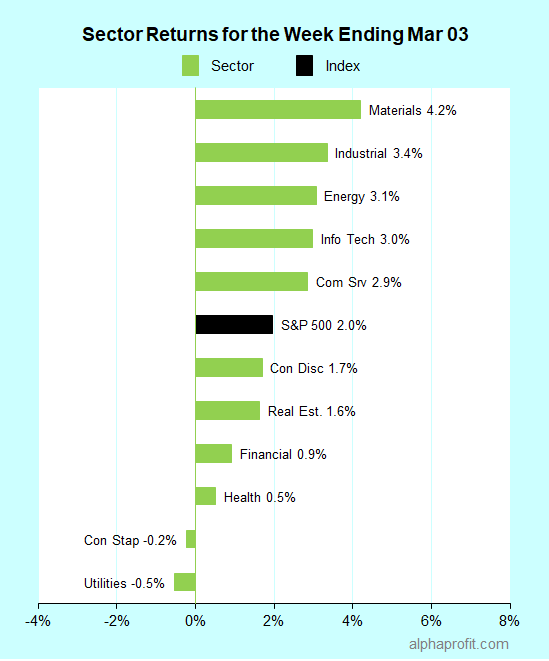

For the week ending March 03, the S&P 500 (SPY) rose 2.0%. Nine of the 11 sectors advanced. Materials (XLB) gained the most, while utilities (XLU) lost the most.

Leading and lagging sectors for the week ending March 03, 2023.

The S&P 500’s top 10 winners included the following:

1. Information Technology Sector

First Solar (FSLR) +30% – The week’s top performer in the S&P 500.

Salesforce (CRM) +15%

SolarEdge Technologies (SEDG) +10%

2. Materials Sector

Steel Dynamics (STLD) +15%

Mosaic (MOS) +11%

3. Health Care Sector

Dentsply Sirona (XRAY) +13%

Illumina (ILMN) +13%

DexCom (DXCM) +12%

4. Consumer Discretionary Sector

Ford Motor (F) +10%

Wynn Resorts (WYNN) +10%

Top ETFs for the week

The following ETF themes worked well: energy, natural gas, solar, metals, mining, copper, and China Internet. The top ETFs for the week include:

United States Natural Gas Fund, LP (UNG) +16.4%

Global X Copper Miners ETF (COPX) +9.9%

SPDR S&P Metals and Mining ETF (XME) +9.8%

KraneShares CSI China Internet ETF (KWEB) +9.5%

Invesco Solar ETF (TAN) +7.7%

Can the S&P 500 push toward 4,200?

* Last week’s late rally pushed the S&P 500 above its 50- and 200-day moving averages. The S&P 500 has ranged between 3,800 and 4,200 in 2023. Can the jobs data and Powell’s testimony this week keep the rally going for the S&P 500 to push toward the top of this trading range?

* The labor market will be in the spotlight next week with the job openings survey on Wednesday and the February employment report on Friday. TradingEconomics.com forecasts job vacancies in the job openings survey to fall to 10.6 million in January from 11.0 million in December. Economists surveyed by Dow Jones predicted the U.S. economy added 225,000 jobs in February. In comparison, the economy added 517,000 jobs in January.

* The Federal Reserve Chairman, Jerome Powell, will testify before Congress on monetary policy on Tuesday and Wednesday. Market participants now expect the Fed to implement four more 0.25% increases in the federal funds rate this year, resulting in a terminal interest rate of 5.50–5.75% in September. Market participants will look to Powell’s testimony to validate the above expectations.

* Three consumer companies in the S&P 500 will report earnings this week. They are Brown-Forman, Campbell Soup, and Ulta Beauty.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

The S&P 500 fell below the 4,000 mark for the first time since January, marking its third straight weekly loss. Stocks fell after the Fed’s preferred inflation measure exceeded economists’ forecasts, and leading retailers lowered their earnings projections. Investors will get plenty of input from Fed officials this week, with many scheduled to speak at engagements. Earnings reports from many retailers are also due.

U.S. stocks fell sharply last Friday after the core Personal Consumption Expenditures (PCE) price index exceeded economists’ forecasts in January.

The core PCE price index, the Fed’s preferred inflation measure that excludes food and energy expenditures, rose 0.6% in January, reflecting a rise of 4.7% over the past 12 months. Economists polled by Dow Jones had forecast the core PCE price index to rise 0.5% in January and 4.4% year over year.

Meanwhile, consumer spending rose 1.8% in January, exceeding economists’ forecast for a 1.3% increase.

The thought of inflation proving sticky worried investors. They feared the Federal Reserve would continue raising its federal funds rate well above 5% to bring down inflation.

Earlier last week, minutes from the Fed’s Jan. 31-Feb. 1 meeting showed officials agreeing that inflation remains well above the central bank’s 2% target. The bank’s officials also agreed on a tight labor market contributing to upward wage and price pressures.

Stocks fell at the start of the week after retailers provided bleak profit forecasts. Walmart lowered its full-year earnings guidance. The retailer said it expects higher-than-expected food inflation to pressure its profit margin. Home Depot warned of weakening demand and issued a grim 2023 profit forecast.

Earnings from semiconductor chipmaker NVIDIA provided some short-lived cheer. The company reported a surge in the use of its chips to power artificial intelligence services.

The yield on the two-year Treasury note ended the week at a four-month high of 4.78%. The 10-year note yielded 3.95%. The yield curve stayed steeply inverted at -0.83%.

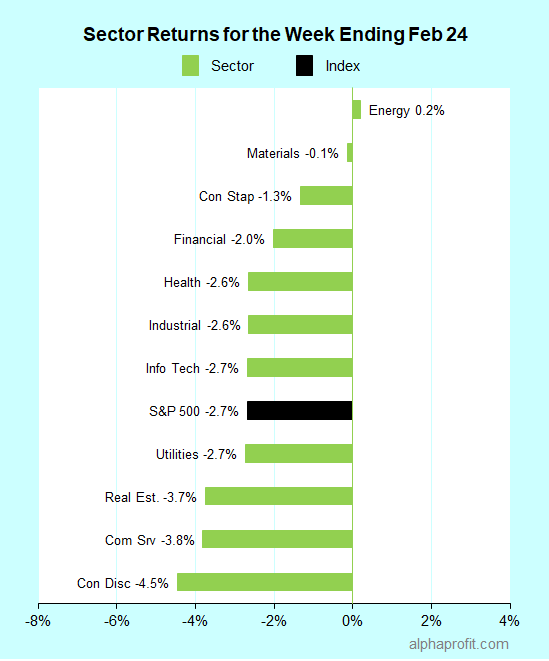

For the week ending February 24, the S&P 500 (SPY) fell 2.7%. Ten of the 11 sectors declined, with energy (XLE) being the exception. Consumer discretionary (XLY) lost the most.

Leading and lagging sectors for the week ending February 24, 2023.

The S&P 500’s top 10 winners included the following:

1. Energy Sector

EQT Corp., (EQT) +9% – The week’s top performer in the S&P 500.

Coterra Energy (CTRA) +4%

2. Materials Sector

Linde PLC (LIN) +7%

3. Consumer Staples Sector

General Mills (GIS) +7%

Molson Coors Beverage (TAP) +5%

Campbell Soup (CPB) +4%

4. Information Technology Sector

ANSYS (ANSS) +7%

NVIDIA Corp. (NVDA) +6%

5. Health Care Sector

GE HealthCare Technologies (GEHC) +6%

Bio-Rad Laboratories (BIO) +5%

Top ETFs for the week

The following ETF themes worked well: energy, natural gas, oil & gas exploration and production, U.S. dollar, consumer staples, food, and beverage. The top ETFs for the week include:

United States Natural Gas Fund (UNG) +9.4%

SPDR S&P Oil & Gas Exploration & Production ETF (XOP) +2.7%

First Trust Energy AlphaDEX Fund (FXN) +2.7%

Invesco DB US Dollar Index Bullish Fund (UUP) +1.4%

First Trust Nasdaq Food & Beverage ETF (FTXG) +0.6%

Will Fed Comments and Retailer Earnings Sink Stocks?

* The S&P 500 fell below the 4,000 mark for the first time since January last week, closing fractionally above its 200-day moving average. Higher-than-expected inflation and lowered earnings projections from leading retailers weighed on stocks. Stocks could come under renewed pressure this week as several Fed officials speak and many retailers report earnings.

* Several Federal Reserve officials speak at engagements this week. The speakers include Fed Governors Bowman, Jefferson, and Waller and the Presidents of the Chicago, Dallas, and Minneapolis Federal Reserve banks. Investors will seek clues on the size of the next interest rate hike and the terminal fed funds rate after the core PCE price index exceeded economists’ forecast last Friday.

* The Institute of Supply Management’s reports on February factory and service activity indexes are arguably the main economic data points of the week. Investors will also receive updates on February consumer confidence from the Conference Board, January home prices from S&P Global, and weekly jobless claims from the Labor Department.

* Twenty-eight S&P 500 member companies report their quarterly earnings this week. The earnings reports from Costco, Lowe’s, Target, and specialty retailers AutoZone, Ross Stores, and Best Buy should provide investors with insights into consumer spending. Investors will also get a pulse on technology spending by enterprises when Broadcom and Salesforce report.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks moved choppily this week. Investors worried that high inflation, a tight job market, and resilient consumer spending would prompt the Fed to pursue a restrictive interest rate policy. The President’s Day holiday on Monday shortens this trading week. The highlight of this short week is the update on the Fed’s preferred inflation measure for January.

U.S. stocks moved choppily this week as economic data gave investors angst.

Inflation in consumer as well as wholesale prices topped economists’ forecasts. The U.S. core consumer price index, which excludes food and energy components, rose 0.4% in January, marking a 5.6% increase from a year ago. Economists surveyed by Dow Jones expected increases of 0.3% and 5.5%, respectively.

The U.S. producer price index, which tracks inflation in wholesale prices, rose at the highest rate in seven months. The PPI rose 0.7% in January, topping economists’ forecast for a 0.4% increase.

Meanwhile, other economic reports showed that consumer spending is strong, and the labor market is tight. The Commerce Department reported that retail sales surged 3.0% in January, compared to economists’ 1.9% growth forecast. The Labor Department showed that the initial claims for unemployment benefits dipped by 1,000 to 194,000 for the week ending February 11.

Several Fed officials expressed concern that inflation is not subsiding quickly enough, implying the central bank needs to continue hiking interest rates.

Market participants raised their expectations for the terminal interest rate to the 5.25–5.50% range. They also upped their forecasts for interest rates to remain high through 2023.

The yield on the 10-year Treasury note rose by 0.09% to close the week at 3.83%.

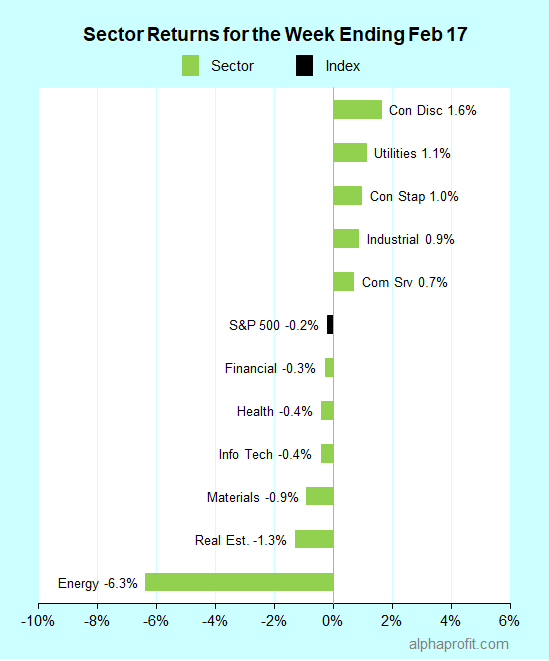

For the week ending February 17, the S&P 500 (SPY) fell 0.2%. Five of the 11 sectors gained. Consumer discretionary (XLY) gained the most, while energy (XLE) lost the most.

Leading and lagging sectors for the week ending February 17, 2023.

The S&P 500’s top 10 winners included the following:

1. Healthcare Sector

West Pharmaceutical, (WST) +16% – The week’s top performer in the S&P 500.

Zoetis (ZTS) +9%

Illumina (ILMN) +8%

2. Materials Sector

Ecolab (ECL) +11%

3. Communication Services Sector

Paramount Global (PARA) +10%

Warner Bros. Discovery (WBD) +9%

4. Industrial Sector

Generac Holdings (GNRC) +9%

5. Consumer Discretionary Sector

Norwegian Cruise Line Holdings (NCLH) +9%

6. Information Technology Sector

Analog Devices (ADI) +8%

Cisco Systems (CSCO) +7%

Top ETFs for the week

The following ETF themes worked well: cryptocurrencies, bitcoin, high-growth companies, innovation, fintech, foreign stocks, Mexico, and France. The top ETFs for the week include:

ProShares Bitcoin Strategy ETF (BITO) +14.6%

ARK Innovation ETF (ARKK) +6.9%

ARK Fintech Innovation ETF (ARKF) +4.3%

iShares MSCI Mexico ETF (EWW) +4.0%

iShares MSCI France ETF (EWQ) +3.1%

Inflation To Stay in Focus This Week

* The Bureau of Economic Analysis (BEA) will release the Personal Consumption Expenditures (PCE) Price Index for January on Friday. Economists surveyed by Dow Jones expect inflation to continue trending lower. They expect the core PCE price index, which excludes food and energy costs, to rise 4.3% year-over-year in January, down from 4.4% in December.

* The fourth-quarter earnings reporting season is coming to an end. The S&P 500 members reporting this week include a mix of consumer, healthcare, and technology names such as Walmart, Home Depot, Booking Holdings, Medtronic, Moderna, NVIDIA, and Intuit.

* Minutes from the Federal Reserve’s recent interest rate policy meeting are due on Wednesday. The Fed raised the federal funds’ benchmark interest rate by 0.25% to the 4.50-4.75% range after this meeting ended on February 1.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Stocks snapped their two-week rally. Rising Treasury bond yields and subpar earnings pressured stocks amid calls for higher interest rates from Fed officials. Investors await the January consumer price index report this week. Earnings reports from about 60 S&P 500 members are due.

Following the previous Friday’s surprisingly strong January jobs report, several Federal Reserve officials voiced their support for higher interest rates. They said additional interest rate hikes were needed to control inflation.

Speaking to the Economic Club of Washington, Fed Chair Jerome Powell said, “The disinflationary process, the process of getting inflation down, has begun, and it’s begun in the goods sector.” Powell cautioned that we are in the early stages of disinflation and have a long way to go.

Referring to the January jobs report, Powell said, “We didn’t expect it to be this strong.” He said the jobs data show why the disinflation process will take quite some time.

The Treasury security auction saw tepid demand from investors in the wake of concerns over rising interest rates. Yields on the 10-year Treasury note surged by 0.22% to 3.74%, their highest in more than a month.

The fourth-quarter earnings reporting season moved forward. By the end of the week, nearly 70% of the S&P 500 companies had reported earnings, giving investors a relatively complete picture.

Analysts labeled the fourth quarter earnings reporting season “underwhelming.” Only 70% of the S&P 500 members reporting earnings have topped analysts’ forecasts. In comparison, 77% and 73% of the index members have exceeded earnings forecasts over the past 5 and 10 years, respectively.

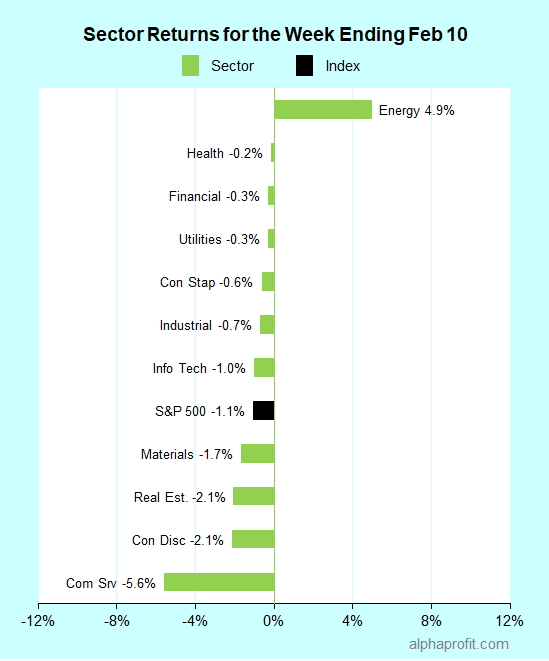

For the week ending February 10, the S&P 500 (SPY) fell 1.1%. Ten of the 11 sectors declined, with energy being the only gainer. Communication services (XLC) lost the most.

Leading and lagging sectors for the week ending February 10, 2023.

The S&P 500’s top 10 winners included the following:

1. Healthcare Sector

Catalent, (CTLT) +26% – The week’s top performer in the S&P 500.

DexCom (DXCM) +9%

2. Information Technology Sector

Fortinet FTNT 12%

Fiserv FISV 8%

Monolithic Power Systems MPWR 8%

3. Financial Sector

Everest Re Group RE 11%

Cincinnati Financial CINF 9%

4. Energy Sector

Phillips 66 PSX 9%

Diamondback Energy FANG 8%

EOG Resources EOG 8%

Top ETFs for the week

The following ETF themes worked well: energy including oil, natural gas, oil & gas exploration & production, and integrated oil. The top ETFs for the week include:

United States Oil Fund, LP (USO) 8.5%

United States Natural Gas Fund, LP (UNG) 7.3%

iShares U.S. Oil & Gas Exploration & Production ETF (IEO) 5.5%

iShares Global Energy ETF (IXC) 5.3%

Energy Select Sector SPDR Fund (XLE) 4.9%

Will CPI Pressure Stocks Further?

* The update on inflation at the retail level is the main event of the week. The Bureau of Labor Statistics will publish the January Consumer Price Index (CPI) on Tuesday. Economists surveyed by Dow Jones expect the core CPI (excluding food and energy prices) to rise 0.3% month-over-month and 5.4% year-over-year, compared to increases of 0.3% and 5.7%, respectively, in December.

* Updates on several other economic measures are also due this week. They include the producer price index, retail sales, housing starts, and the Conference Board’s U.S. leading economic index.

* The fourth-quarter earnings reporting season is in its home stretch. Earnings reports from nearly 60 S&P 500 members are due this week. Applied Materials, Cisco Systems, Coca-Cola, and Deere are among the companies reporting.

* The U.S. Senate Committee on Banking, Housing, and Urban Affairs will hold a hearing on cryptocurrencies and digital assets.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

ETFs focusing on Ethereum and high-growth companies involved in battery technologies, electric vehicles, autonomous vehicles, and clean energy were top performers in January.

Top Performing ETFs for January 2023

Excludes ETFs leveraged or less than $500 million in assets

* Grayscale Ethereum Trust, ETHE +54.6%

* ARK Innovation ETF, ARKK +27.8%

* Global X Lithium & Battery Tech ETF, LIT +20.7%

* Invesco WilderHill Clean Energy ETF, PBW +20.1%

* Global X Autonomous & Electric Vehicles ETF, DRIV +19.6%

Stocks contributing to the performance of the above ETFs likely include Albemarle (ALB), Archer Aviation (ACHR), Block (SQ), Coinbase Global (COIN), Energy Vault (NRGV), EVgo (EVGO), Exact Sciences (EXAS), FuelCell Energy (FCEL), Navitas Semiconductor (NVTS), NVIDIA Corp. (NVDA), QuantumScape (QS), Roku (ROKU), Solid Power (SLDP), Teladoc Health (TDOC), Tesla (TSLA), and TPI Composites (TPIC).

Stay on top of the stock market with ‘Looking Back, Looking Forward’

U.S. stocks extended their gains after the Fed raised interest rates by 0.25%, as expected, and Chair Powell said the disinflationary process has started. The job market continued to exhibit vigor, while earnings from Alphabet, Amazon, and Apple disappointed investors. Investors will scrutinize earnings reports from about 90 S&P 500 members this week.

Last Wednesday, the Federal Reserve’s interest rate policy committee raised the benchmark federal funds interest rate by 0.25% to the 4.50-4.75% range. Market participants widely anticipated this outcome.

Comments from Chairman Jerome Powell on disinflation came as a relief to investors. Powell said, “We can now say for the first time that the disinflationary process has started.”

The Fed did not provide a timeline on when it may pause interest rate increases. The central bank said ongoing increases in interest rates would be needed to return inflation to its 2.0% long-term goal over time.

The European Central Bank and the Bank of England followed the Fed, raising their benchmark interest rates by 0.5%, in line with economists’ expectations.

Data from the job market continued to be a bastion of strength. The U.S. economy added 517,000 jobs in January, well above economists’ forecast of 187,000. The unemployment rate fell to 3.4%, its lowest since 1969. Average hourly earnings rose 0.3%, in line with expectations. Additionally, job openings surged in December to 11.0 million from 10.4 million in November.

In other economic reports, the Institute for Supply Management’s (ISM) manufacturing index declined more than economists expected to 47.4 in January from 48.4 in December. The ISM’s services activity index rebounded sharply to 55.2 in January from 49.6 in December. Economists had forecasted 50.6.

Marquee companies reported mixed earnings. Facebook-parent Meta Platforms fared well, while Alphabet, Amazon, and Apple fell short of analysts’ expectations.

Enduring strength in stock prices pushed the S&P 500’s 50-day moving average above its 200-day moving average last Thursday, forming a “golden cross.” Chart analysts see the golden cross as a bullish signal.

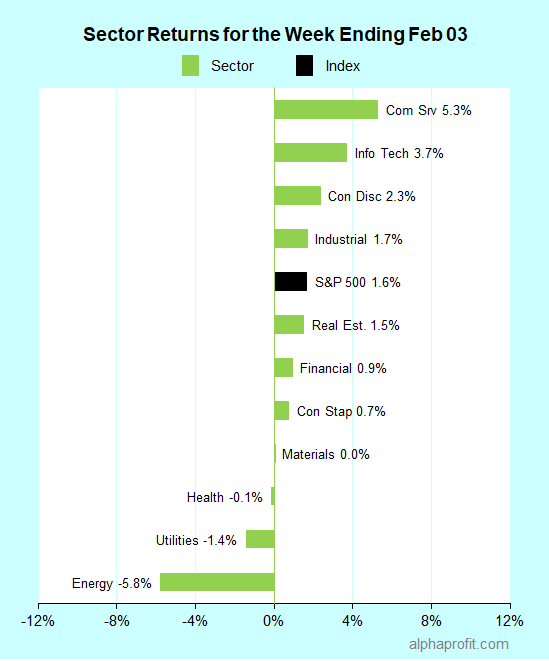

For the week ending February 03, the S&P 500 (SPY) rose 1.6%. Eight of the 11 sectors advanced. Communication services (XLC) gained the most, while energy (XLE) lost the most.

Leading and lagging sectors for the week ending February 03, 2023.

The S&P 500’s top 10 winners included the following:

1. Healthcare Sector

Align Technology, (ALGN) +27% – The week’s top performer in the S&P 500.

Stryker Corp. (SYK) +11%

2. Communication Services Sector

Meta Platforms (META) +23%

3. Industrial Sector

W.W. Grainger (GWW) +18%

Pentair PLC (PNR) +15%

A. O. Smith Corp. (AOS) +14%

FedEx Corp. (FDX) +13%

4. Information Technology Sector

Advanced Micro Devices (AMD) +14%

5. Consumer Discretionary Sector

CarMax (KMX) +13%

PulteGroup (PHM) +12%

Top ETFs for the week

The following ETF themes worked well: smallcaps, banking, innovation, homebuilders, and transportation. The top ETFs for the week include:

Invesco S&P SmallCap 600 Revenue ETF (RWJ) 6.2%

SPDR S&P Regional Banking ETF (KRE) 6.2%

ARK Innovation ETF (ARKK) 6.1%

SPDR S&P Homebuilders ETF (XHB) 6.0%

iShares Transportation Average ETF (IYT) 5.9%

What’s Next after the Golden Cross

* Investors will look for the rally in stocks to continue after the S&P 500 index successfully formed a “golden cross” last week.

* Corporate earnings will be in the spotlight this week. Nearly 90 of the S&P 500 index members report earnings. AbbVie, CVS Health, Disney, Linde PLC, PayPal Holdings, PepsiCo, and S&P Global are some of the widely followed names on this week’s earnings calendar.

* The University of Michigan releases its preliminary January consumer sentiment reading along with inflation expectations on Friday. Economists surveyed by Dow Jones expect consumer sentiment to rise and inflation expectations to fall.

* Jobless claims numbers are likely to get more scrutiny than they usually do. Investors will likely seek confirmation of the labor market’s robustness in the jobless claims data after job creation in January topped economists’ forecasts by a wide margin last Friday.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

U.S. stocks rose last week after inflation data suggested the Fed is succeeding in quelling price increases without much damage to the economy. Investors took the year-over-year decline in earnings in stride, believing it would provide less room for the Fed to raise interest rates. The S&P 500 is just a few points away from forming a bullish golden cross. The week ahead includes the Fed meeting, earnings, and the jobs report.

December inflation data suggested that the Federal Reserve is succeeding in curbing price increases without a material increase in unemployment. The Fed’s preferred inflation measure, the core Personal Consumption Expenditures (PCE) price index, which excludes food and energy prices, rose 4.4% in the year through December. In the 12 months through November, the core PCE price index had risen 4.7%.

Gross domestic product growth in the fourth quarter exceeded economists’ forecasts. The Bureau of Economic Analysis (BEA) reported the economy expanded at an annualized rate of 2.9% during the fourth quarter. Economists surveyed by Dow Jones expected the GDP to grow by 2.8%.

Over 100 members of the S&P 500 index reported their fourth-quarter earnings last week, completing the first third of the reporting season. According to FactSet, nearly 70% of reporting companies have exceeded analysts’ EPS forecasts. The aggregate earnings for the S&P 500 index are on track to decline 5% year over year. Investors have perceived the decline in earnings as good news since it may leave less room for the Fed to raise interest rates.

For the week ending January 27, the S&P 500 (SPY) rose 2.5%. Nine of the 11 sectors advanced. Consumer discretionary (XLY) gained the most, while healthcare (XLV) lost the most.

Leading and lagging sectors for the week ending January 27, 2023.

The S&P 500’s top 10 winners included the following:

1. Consumer Discretionary Sector

Tesla, (TSLA) +33% – The week’s top performer in the S&P 500.

2. Information Technology Sector

Western Digital (WDC) +17%

Seagate Technology (STX) +16%

NVIDIA Corp. (NVDA) +14%

3. Communication Services Sector

Warner Bros. Discovery (WBD) +15%

Paramount Global (PARA) +14%

4. Financial Sector

American Express (AXP) +14%

Capital One Financial (COF) +13%

5. Materials Sector

Albemarle (ALB) +13%

5. Industrial Sector

United Rentals (URI) +13%

Top ETFs for the week

The following ETF themes worked well: innovation, clean energy, lithium, battery technologies, cloud computing, autonomous technology, and robotics. The top ETFs for the week include:

ARK Innovation ETF (ARKK) 10.7%

First Trust NASDAQ Clean Edge Green Energy (QCLN) 9.3%

* Last week’s rally in the S&P 500 brought the benchmark’s 50- and 200-day moving averages (DMAs) within 15 points or 0.4% of each other. Wall Street has a busy week ahead. The week includes the Fed’s interest rate policy meeting, several earnings reports, and the January jobs report. Investors are eager to see if these events can facilitate a bullish “golden cross” in the S&P 500, with the 50-DMA rising above the 200-DMA.

* The Federal Reserve’s interest rate policy meeting on Tuesday and Wednesday is the most widely anticipated event of the week. Economists surveyed by Dow Jones expect the Fed to raise the benchmark federal funds interest rate by 0.25% to the 4.50-4.75% range at the end of this meeting. Some investors also expect the Fed to signal a pause in interest rate increases during the spring months after the Wall Street Journal raised this possibility last week.

* Another busy week lies ahead on the earnings front. The S&P 500 index heavyweights Alphabet, Amazon, and Apple report earnings this week. The earnings calendar includes reports from many more household names, including ExxonMobil, Facebook-parent Meta Platforms, McDonalds, and Pfizer.

* The Labor Department releases the January jobs report on Friday. Economists surveyed by Dow Jones forecast the U.S. economy to have added 190,000 jobs in January, down from 223,000 in the previous month. They expect the unemployment rate to rise to 3.6% from 3.5%.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

U.S. stocks fell to post their first loss of the year as investors worried about a recession. The deterioration in measures of manufacturing and retailing activities exceeded economists’ expectations. The earnings reporting season gathers steam this week. Investors will receive updates on growth and inflation measures.

Last week, economic growth indicators raised the specter of a recession. The New York Fed’s Empire State Manufacturing Survey fell sharply in January, suggesting a contraction in manufacturing. Orders fell, while employment growth stalled.

Separately, retail sales dropped 1.1% in December as consumer spending slowed. The decline in retail sales exceeded economists’ 1.0% forecast.

The mixed quality of fourth-quarter earnings reports offered little to alleviate recession worries. Investors bid up the shares of Morgan Stanley and Netflix after the companies reported earnings. Conversely, shares of Charles Schwab, Goldman Sachs, and Procter & Gamble fell.

The labor market, however, continued to remain vibrant, showing no signs of slowing. Weekly jobless claims fell, pointing towards continued tightness.

Inflation data comforted investors. The producer price index declined 0.5% in December, well above economists’ forecast for a decline of 0.1%. Price measures in the New York Fed’s Manufacturing Survey indexes fell.

Although inflation continued to moderate, Federal Reserve officials did not signal an intent to halt interest rate increases. Instead, they appeared inclined to slow the pace of interest rate increases. Investors fretted that a tight job market would encourage the Fed to raise interest rates more than needed.

The U.S. hit its $31.4 trillion debt ceiling last Thursday. The Treasury Department began to use a series of “extraordinary measures” to avoid a government debt default. These measures give the U.S. until June to either raise the debt ceiling, suspend the debt ceiling, or figure another way out.

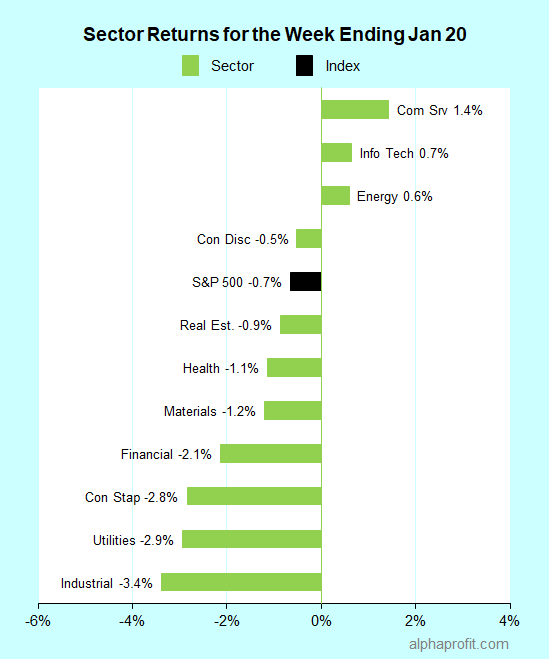

For the week ending January 20, the S&P 500 (SPY) fell 0.7%. Three of the 11 sectors advanced. Communication Services (XLC) gained the most, while industrials (XLI) lost the most.

Leading and lagging sectors for the week ending January 20, 2023.

The S&P 500’s top 10 winners included the following:

1. Financial Sector

SVB Financial Group, (SIVB) +15% – The week’s top performer in the S&P 500.

Signature Bank (SBNY) +9%

First Republic Bank (FRC) +7%

2. Health Care Sector

ResMed (RMD) +10%

3. Communication Services Sector

Match Group (MTCH) +9%

Alphabet (GOOG) +8%

4. Information Technology Sector

NVIDIA Corp. (NVDA) +8%

ServiceNow (NOW) +7%

5. Consumer Discretionary Sector

Expedia Group (EXPE) +8%

Tesla (TSLA) +8%

Top ETFs for the week

The following ETF themes worked well: bitcoin, carbon credits, Indonesia, Japan, and fintech. The top ETFs for the week include:

ProShares Bitcoin Strategy ETF (BITO) 14.6%

KraneShares Global Carbon ETF (KRBN) 4.2%

iShares MSCI Indonesia ETF (EIDO) 3.6%

WisdomTree Japan Hedged Equity Fund (DXJ) 3.1%

ARK Fintech Innovation ETF (ARKF) 3.0%

Will 4Q2022 Earnings Pull Stocks Out of Malaise?

* Stocks are stuck in a trading range. The S&P 500 has ranged between 3,750 and 4,100 since the start of 2023. Stock prices have fluctuated as investor confidence in the Federal Reserve’s ability to lower inflation without causing a recession has waxed and waned.

* A busy week lies ahead on the earnings front. Over 100 members of the S&P 500 index, including six of the 20 top constituents, report quarterly earnings. They are Chevron, Johnson & Johnson, Mastercard, Microsoft, Tesla, and Visa.

* The Bureau of Economic Analysis (BEA) will release the Personal Consumption Expenditures (PCE) Price Index for December on Friday. Economists surveyed by Dow Jones expect inflation to continue trending lower. They expect the core PCE price index, which excludes food and energy costs, to rise 4.4% year-over-year in December, down from 4.7% in November.

* The BEA will also release its preliminary gross domestic product growth estimate for the final quarter of 2022. Economists surveyed by Dow Jones expect the pace of expansion to slow to a seasonally adjusted annual rate of 2.8% from 3.2% in the third quarter.

* The debt ceiling has been pushed into the background for now. House Republicans want to cut government programs before they approve a higher ceiling. So far, the White House has refused to negotiate with hardline Republicans, believing the latter would eventually back off their demands due to pressure from conservative & moderate Republicans and business groups. However, the risk of a decline in stock prices would rise if the debt ceiling remained unresolved until the last minute in June.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

The S&P 500 gained for a second straight week after leading banks reported fourth-quarter earnings in line with investors’ expectations. Inflation continued to moderate, raising hopes that the Fed would increase interest rates gradually. The markets are open for trading four days this week, shortened by Martin Luther King Jr. Day on Monday. Congress needs to address the U.S. debt ceiling to avoid a default. The fourth-quarter earnings reporting season continues this week. Investors will also get an update on wholesale price inflation.

The S&P 500 posted its second consecutive week of gains, recording its best weekly performance since November.

Leading banks kicked off the fourth quarter earnings reporting season. The CEOs of JPMorgan Chase, Bank of America, and Citigroup said they anticipate a “mild recession.”

Investors were unfazed, taking this assessment as expected.

Inflation data raised hopes of the Federal Reserve less aggressively increasing interest rates.

Helped by a sharp decline in gasoline prices in December, U.S. consumer prices fell for the first time in more than 2-1/2 years. The consumer price index dropped 0.1% to show a 12-month increase of 6.5%.

The core CPI, which excludes food and energy prices, rose 0.3% last month, in line with economists’ expectations. The 5.7% increase in the core CPI on a 12-month basis also matched economists’ forecasts.

St. Louis Federal Reserve Bank President James Bullard said the probability of an economic soft landing has increased due to “encouraging” inflation data.

In other data, the University of Michigan consumer sentiment survey showed the one-year inflation outlook slowed to 4%, the lowest level since April 2021.

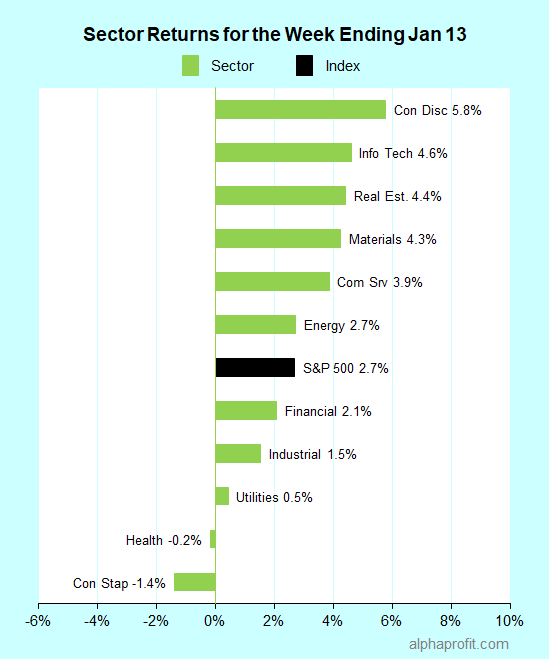

For the week ending January 13, the S&P 500 (SPY) rose 2.7%. Nine of the 11 sectors advanced. Consumer discretionary (XLY) gained the most, while consumer staples (XLP) lost the most.

Leading and lagging sectors for the week ending January 13, 2023.

The S&P 500’s top 10 winners included the following:

1. Industrial Sector

United Airlines, (UAL) +22% – The week’s top performer in the S&P 500.

American Airlines (AAL) +20%

2. Consumer Discretionary Sector

Norwegian Cruise Line Holdings (NCLH) +20%

Royal Caribbean Cruises (RCL) +15%

Carnival Corporation (CCL) +14%

Amazon.com (AMZN) +14%

3. Communication Services Sector

Warner Bros. Discovery (WBD) +16%

4. Information Technology Sector

First Solar (FSLR) +15%

NVIDIA Corp. (NVDA) +14%

ServiceNow (NOW) +13%

Top ETFs for the week

The following ETF themes worked well: airlines, bitcoin, and high-growth groups such as innovation, clean energy, and cloud computing. The top ETFs for the week include:

ProShares Bitcoin Strategy ETF (BITO) 16.0%

Invesco WilderHill Clean Energy ETF (PBW) 14.8%

ARK Innovation ETF (ARKK) 14.7%

U.S. Global Jets ETF (JETS) 9.4%

WisdomTree Cloud Computing Fund (WCLD) 8.3%

Will 4Q2022 Earnings Offset the Debt Ceiling Worry?

* The debt ceiling is back in the spotlight. Treasury Secretary Janet Yellen has said the U.S. would hit the statutory debt limit this week. Congress needs to either raise or suspend the debt ceiling. A quick resolution to the debt ceiling issue is hardly a foregone conclusion. Recently, the House of Representatives voted 15 times before confirming Kevin McCarthy as Speaker. Yellen has said the Treasury Department will “begin taking extraordinary measures to prevent the U.S. from defaulting on its debt obligations.”

* Fourth-quarter earnings reports continue this week. Leading companies from other industries will report earnings alongside financial firms Morgan Stanley, Goldman Sachs, and PNC Bank. They include Netflix, Procter & Gamble, PPG Industries, and Schlumberger.

* Updates on two widely followed economic measures are due this week. First, the U.S. Census Bureau’s December retail sales report should provide insights into consumer spending during the 2022 holiday season. Second, investors will look for signs of continued slowing in wholesale price inflation when the Bureau of Labor Statistics releases the December Producer Price Index.

Stay on top of the stock market with ‘Looking Back, Looking Forward’

Sign up for the FREE investment newsletter AlphaProfit Money Matters and immediately receive Two Special Reports

Five Smart Ways to Profit from Sector Funds and ETFs

Avoid Three Common Mistakes ETF Investors Make

Don’t miss timely investment tips. Stay ahead of the market with AlphaProfit MoneyMatters in your inbox

Premium Service Performance

Model Portfolio Annualized Returns

DEC. 1993 to DEC. 2025

Fidelity Agg. Growth

17.6%

Fidelity Growth

14.6%

ETF Agg. Growth

17.4%

ETF Growth

14.4%

ETF Style Rot. (since 2009)

11.3%

S&P 500

10.8%

Stock Recommendation Returns

DEC. 2013 to DEC. 2025

Win Rate

91%

Avg. Holding Period

2.6 months

Avg. Gain

13.1%

MEET

DR. SAM SUBRAMANIAN

Sam Subramanian PhD, MBA has credentials that are the envy of most investment advisers. He combines strong quantitative skills with deep financial expertise and insights on inner workings of Wall Street and corporations. His creativity has helped him win 16 U. S. patents.

Prior to founding AlphaProfit Investments, LLC, Sam worked in positions of increasing responsibility in Finance and Corporate Strategy for McKinsey & Company, Exxon Corporation, and Unocal Corporation. His work centered on Acquisitions and Divestitures, Asset Valuation, Trading, Bankruptcies, and Risk Management.

Well aware of the dismal returns produced by money managers, he was determined to take charge of his own investments. He created a low cost, low effort but high return investing system and rigorously tested it for over two decades using his own money.

This high-performance system helped Sam to quickly become financially independent. Sam still invests his money, using the now award-winning system he created. He shares the unbiased, crystal-clear recommendations and market moves with his subscribers.